Yesterday I suggested some specific transparency measures to rebuild trust in light of #SwissLeaks. Today my colleagues at TJN pointed out that they are way ahead of me: here’s how.

#SwissLeaks and accountability

The public revelations led by the ICIJ have laid bare the multiple failures by tax authorities and/or governments in respect of data they either had, or chose not to have, from 2010. I offered this suggestion for transparency measures to rebuild trust and ensure greater accountability:

- Publish data on the aggregate bank holdings in other jurisdictions of residents, as declared by the banks and through automatic information exchange between jurisdictions (in effect, the national components of the locational banking data collected but not published by the Bank for International Settlements, which was called out by the Mbeki panel and African Union last week);

- Publish data on the equivalent, as reported by taxpayers;

- Publish regular updates on the status towards resolution of any discrepancy, e.g. “three cases accounting for 27% of last year’s discrepancy are now being prosecuted; investigations continue into 154 cases which account for a further 68%; while further work is underway to determine the nature of the remainder of the discrepancy (5%).” Addendum: @AislingTax points out quite rightly that I need another category here: the ‘gap’ which is not a gap, but rather relates to other features of the tax system such as non-doms in the UK.

TJN proposal

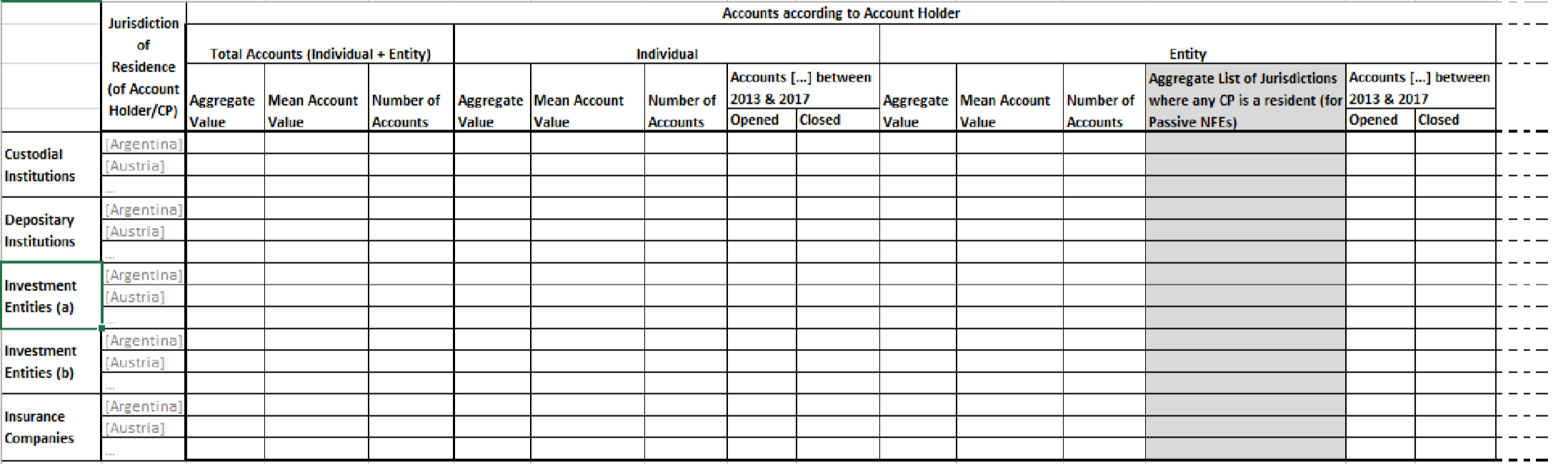

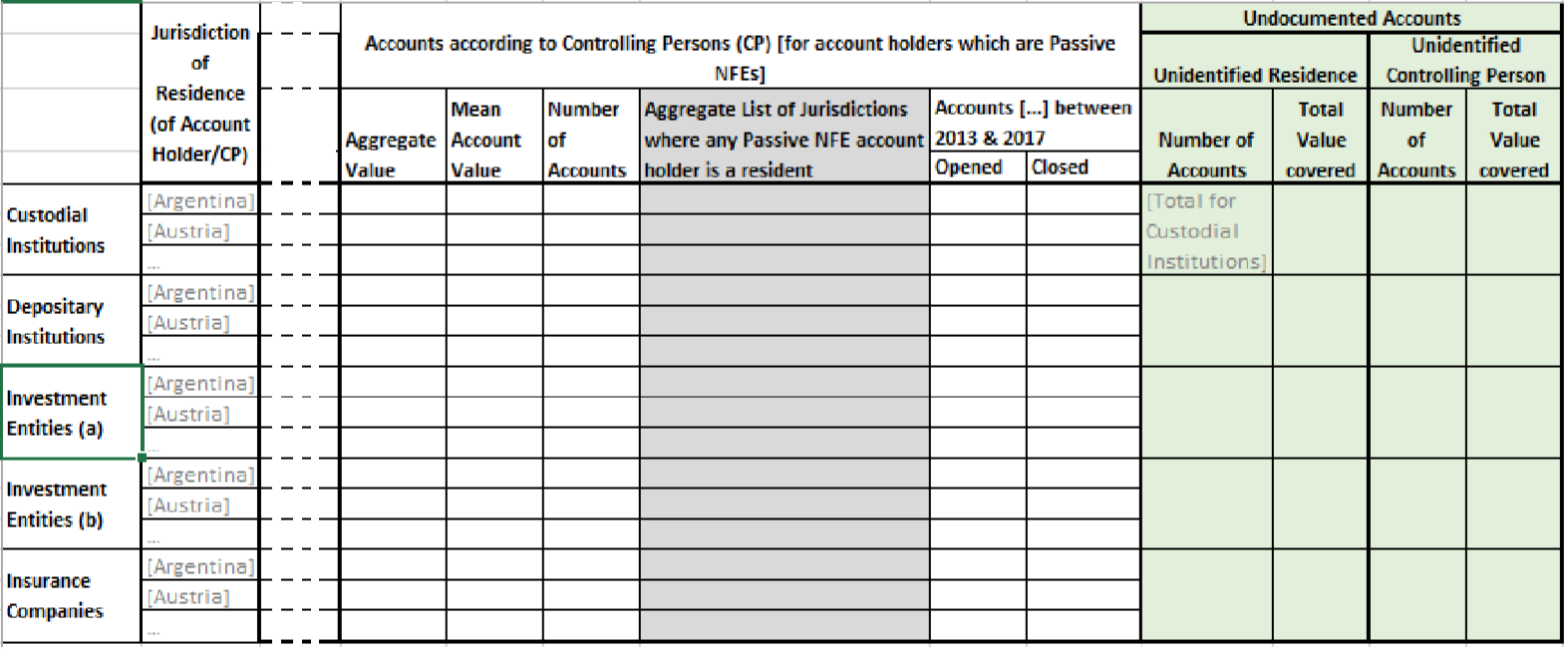

Colleagues at TJN have been discussing for some time how best to provide public information around the emerging mechanisms for automatic exchange of tax information between jurisdictions. Andres Knobel who works from Argentina on the Financial Secrecy Index, drafted an outline template for simple, aggregate data.

It looks something like this (forgive the break for ease of viewing).

The advantage this structure would have over existing data formats (with thanks to Markus Meinzer) is that for the first time, we would be able to find out about the beneficial owners or controlling persons (CP) of assets held via complex trust and shell company structures. So far, the data is limited to legal ownership, which stops at the next lawyer posing as nominee, or the company bought from a shelf in Nirvana land.

Given all the loopholes TJN has identified in the OECD’s Common Reporting Standard (CRS), this data (format) could serve as an important evaluation tool for checking how much of the assets identified through BIS (and other sources) are actually being covered and reported under the CRS. One particularly devious way of escaping the CRS will consist in jurisdictions offering “residency-for-sale” certificates, such as the Bahamas (see also here).

The outline format has recently been shared with the OECD and Global Forum. Comments and suggestions are warmly welcomed.