The UK has successfully defended the ‘patent box’ against the charge that it is a major avenue for multinational corporate tax abuse. Now everybody wants one, even though the evidence suggests that only multinationals will benefit.

Will countries take the last chance for productive cooperation offered by BEPS; or will the patent box end up as the paradigmatic case of rich countries ‘competing’ themselves down (and taking developing countries with them)?

[I’m grateful to Prof. Sol Picciotto, TJN senior adviser and coordinator of the BEPS Monitoring Group, for flagging this issue, and the Tax Notes coverage referred to, and for commenting on a draft.]

The magic of the patent box (montage from Dreamtimes original images)

Where things stand

The term ‘patent box’ is being used more widely than for patent incentives alone, to reflect a range of preferential tax treatments for intellectual property (IP). Such preferential regimes fall under Action 5 of the OECD’s Base Erosion and Profit Shifting (BEPS) Action Plan, which aims to ‘Counter harmful tax practices more effectively, taking into account transparency and substance’, requiring inter alia ‘substantial activity for any preferential regime’.

The first Action 5 report suggests three helpful questions for considering whether a preferential regime such as the patent box is harmful:

Does the tax regime shift activity from one country to the country providing the preferential tax regime, rather than generate significant new activity?

Is the presence and level of activities in the host country commensurate with the amount of investment or income?

Is the preferential regime the primary motivation for the location of an activity?

In general, pre-BEPS patent box regimes would yield the answers ‘Yes’, ‘No’, ‘Yes’: that is, they are indeed ‘harmful’.

But when BEPS got underway and a number of countries saw their measures to attract profit-shifting come under increasing pressure, the UK led a vigorous defence of the patent box (supported by other then-users, Luxembourg, Netherlands and Spain).

Eventually, however, the UK was forced to give a little ground, in the face of some combination of the logic of the BEPS process, in the initiation of which the UK had played a significant role, and pressure from Germany, where finance minister Schäuble has been an implacable opponent.

As Ajay Gupta’s handy piece in Tax Notes International ($) explains, Anglo-German agreement in November 2014 followed the OECD’s September 2014 paper looking at three possible approaches to requiring ‘substantial economic activity’ in relation to the patent box:

Value creation (tax benefits apply only if specific criteria for development activities taking place in the jurisdiction are met);

Transfer pricing (the UK’s preferred approach, requiring the assessment of functions, assets and risks); and

Nexus (the OECD’s preference, limiting ‘tax benefits to the fraction of IP income equal to the ratio of qualifying research expenditures to aggregate expenditures incurred to develop the IP asset’).

Two things about the OECD’s preference are striking. First, what it means: that even with the BEPS context of defending the arm’s length principle and separate accounting against alternatives such as unitary taxation with formulary apportionment, the OECD came out clearly against relying only on a transfer pricing approach to IP. As critics such as the BEPS Monitoring Group have pointed out, allocating profits according to ‘functions, assets and risks’ is inherently subjective and discretionary, so liable to abuse and likely to produce conflict.

Second, the OECD paper set the context for the UK to retreat, at least a little. The Anglo-German compromise, which was immediately taken up by the OECD, was a modified nexus approach: nexus, but as Gupta puts it, ‘allowing a taxpayer to increase its qualifying expenditures above its self-incurred research expenditures by up to 30 percent, a so-called uplift, to reflect expenditures for research activities outsourced to related parties and IP acquisition costs.’ The UK also bought some time, with June 2016 the last date to introduce new, non-conforming provisions, and June 2021 the date for their elimination, as well as some opportunities to ‘grandfather’ existing provisions.

It should also be pointed out that the BEPS project is likely to propose only a toothless monitoring mechanism, through the Forum on Harmful Tax Practices. This consists of government representatives, and operates in total secrecy. The Forum has been in existence for some 15 years and has been largely ineffective – not surprising, as governments have little incentive to oppose a tax break which they themselves support, or might want to introduce. The ‘nexus’ test will require companies to introduce a ‘track and trace’ procedure to prove their expenditures, but this will presumably be checked only by the country providing the tax break. This is a recipe for sweetheart deals as we have already seen with Ireland’s tax breaks for Apple and others, and the Lux Leaks revelations.

Where things are headed

Gupta, and in a related piece ($) his colleague Marty Sullivan, identify the major impacts of the UK-German agreement. Above all, the patent box has been established as a ‘winning’ BEPS strategy: that is, as a mechanism to attract profit-shifting which is acceptable.

Hardly surprising, therefore, that there is now a stampede to introduce such tax breaks, each one tailored slightly differently.

Current providers already include Belgium, Cyprus, France, Hungary, Ireland, Luxembourg, Malta, Netherlands, Spain and of course the UK. Italy is introducing one (which will especially benefit sectors such as luxury goods and fashion), as well as Switzerland (presumably aimed at watches and cuckoo clocks). There is now also active discussion in the United States about joining the bandwagon. As Gupta puts it:

Don’t look now, but the United States just signaled its willingness to enter a race with the European Union for attracting technology investment — a race that will surely end with multinational enterprises walking away with the top prize. As EU jurisdictions fall over each other to adopt patent box regimes and the OECD seems ready to endorse a modified nexus approach for testing the validity of these regimes, the U.S. Senate Finance Committee’s international tax reform working group has recommended the enactment of its own preferential structure for taxing intellectual property income.

Sullivan, meanwhile, reviews the latest academic research carried out for the European Commission. His conclusion? With my emphasis:

Before Congress adopts a multibillion-dollar tax incentive like a patent box, it should have some inkling as to whether it is effective at increasing research. So far the evidence is very sparse, and what little evidence does exist is not favorable. Yes, a U.S. patent box would be likely to increase patent registrations in the United States. But in most cases that would just be legal maneuvering without any corresponding increase in the stuff we really want: scientists doing research and inventors inventing inside our borders.

While the BEPS Action Plan reflects the need for countries to coordinate further to avoid such an outcome, the modified nexus approach simply confirms the futile notion of ‘competition’ on tax, locking in a race to the bottom. As the BEPS Monitoring Group noted presciently in February:

The OECD approach will simply legitimize ‘innovation box’ regimes and hence supply a legal mechanism for profit shifting, encouraging states to provide such benefits to companies. It will be particularly damaging to developing countries, which may be used as manufacturing platforms, while their tax base will be drained by this legitimized profit-shifting. Such measures should simply be condemned and eliminated.

Last chance saloon

All is not yet lost. The OECD has not finally committed to the modified nexus approach, and the US has not yet taken the step to become a patent box ‘competitor’, which would surely make any global step back impossible in the short-medium term at least.

What would it take for the rich countries to save themselves from the more aggressive struggle for each others’ tax base that BEPS was supposed to redress? Or to limit the extent to which international rules support developing country revenue losses (which are indeed substantial)?

Well, the fine details are still under discussion at the OECD: What chance a piece of genuine international leadership from the UK or US, or a rethink by Germany or others on the acceptability of modified nexus versus complete elimination?

A draft paper by Maya Forstater, circulated by the Center for Global Development in time for the Financing for Development conference in Addis, attacks the integrity of many people and NGOs working on tax justice and illicit financial flows.

The claims include:

that (some?) NGOs have “contributed to unrealistic public expectations and an appetite for an overly simplistic narrative about a corporate tax ‘pot of gold’” (p.31);

that (some?) NGOs tolerate “exaggerated interpretations and misunderstandings”(p.33);

that (some?) NGOs do not “engage honestly with debates over economic trade offs [sic]” (p.33); and

that this behaviour is comparable to “the use of exploitative and prejudiced imagery in charity appeals” (p.34).

Blimey.

This is a (really) long post, as I’ll try to cover the breadth and strength of Maya’s many claims. I should say that I took part in the first of two meetings of the group CGD convened to look at the issues. This was really quite a constructive coming together of different viewpoints. But I stood down when the subsequent blog post seemed to ignore most of the common ground and reiterated some earlier attacks on NGOs instead, making some claims about ‘inconvenient truths’ that resurface here. Comparing back, I’m afraid it seems as if the results of the research exercise were pre-determined.

Some main points from the discussion below:

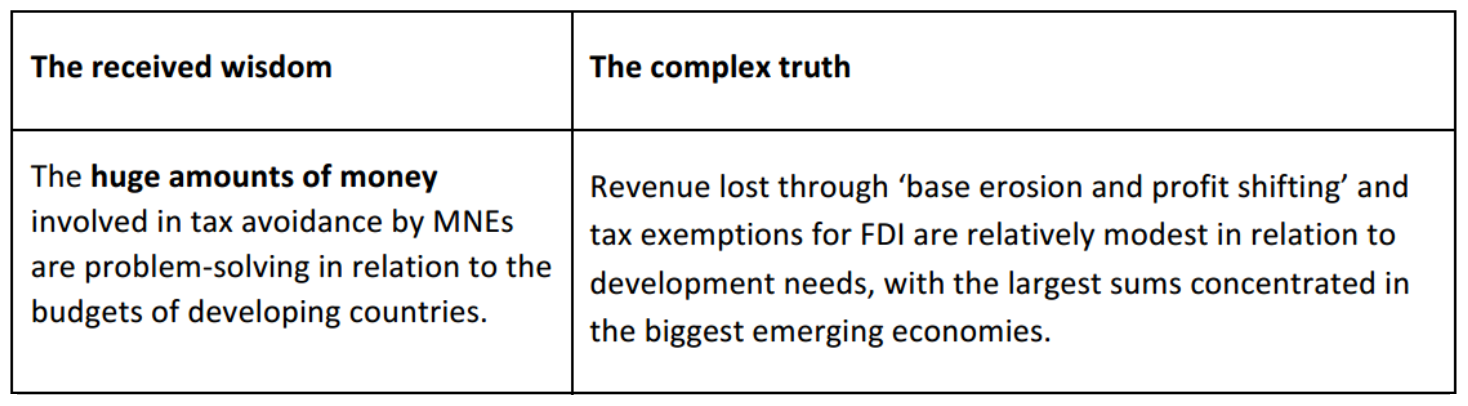

The draft paper makes a series of claims without providing any serious evidence: most importantly, a ‘complex truth’ that tax losses are not of ‘problem-solving’ scale but ‘relatively modest in relation to development needs’. The existing evidence, e.g. from the IMF or – strikingly! – the author’s own analysis in this paper of ActionAid’s work, clearly supports the opposing view.

In the two other cases where ‘received wisdom’ associated with NGOs is contrasted with ‘the complex truth’, there is in fact no direct contradiction – but the presentation in each case creates an implicit straw man of NGO opposition to the truth.

The paper’s main thrust is that there is no ‘pot of gold’ for developing countries – but no substantial evidence is offered to support this assertion. (I’m sympathetic to the idea that this aspect of the tax justice agenda is sometimes overstated, but simply to deny the existing evidence offers no way forward. Indeed this is why I encouraged this work to focus instead on substantive research issues, albeit to no avail.)

I should point out that I was a research fellow at CGD during 2013-2014, and remain grateful to Owen Barder and colleagues for giving me a great deal of space to pursue research in just this area. I hope it may be possible to revise the final draft in such a way that it can make a useful contribution.

Measuring the illicit

The bulk of the attack in the draft paper is dedicated to three elements of ‘received wisdom’, each of which are contrasted with a quite different ‘complex truth’, so I’ll focus on these before coming back to the overarching claims. First, a little bit of context.

As has often been remarked, attempts to estimate illicit financial flows (IFF) are inevitably fraught with difficulty.

By definition, illicit flows are those ‘forbidden by law, rule or custom’: so whether or not they are technically legal, like large-scale tax avoidance, they are always hidden from view where possible. Add to this the fact that the relevant international datasets are often of less than ideal quality and coverage, or sometimes simply held in private by multilateral organisations who should know better, and the problem is of estimating things that are deliberately hidden, on the basis of anomalies in data that are imperfect in any case.

The development of the research field – which has come into being seriously only in the last 15 years – has been led by NGOs, perhaps because academic researchers felt uncomfortable with the degree of uncertainty, or because those at international organisations didn’t see it as a policy priority. At each stage, NGOs and the few academic researchers have challenged international organisations to use their capacity, and ability to access data, to do better; but until this year, there had been no serious response on any aspect of IFF except that of UNODC and the World Bank in their Stolen Assets Recover (StAR) initiative.

Eurodad’s famous 2009 Illicit Financial Flows report, summarising the research contribution of international organisations

Following the G20 meetings in 2009, however, the issues originally promoted by NGOs in the wilderness rocketed to the top of the global agenda. Then in 2013, the G8 and G20 commissioned the OECD to carry out the Base Erosion and Profit Shifting initiative (BEPS), aimed at reducing the misalignment between the location of multinational companies’ economic activity, and where they declare taxable profits.

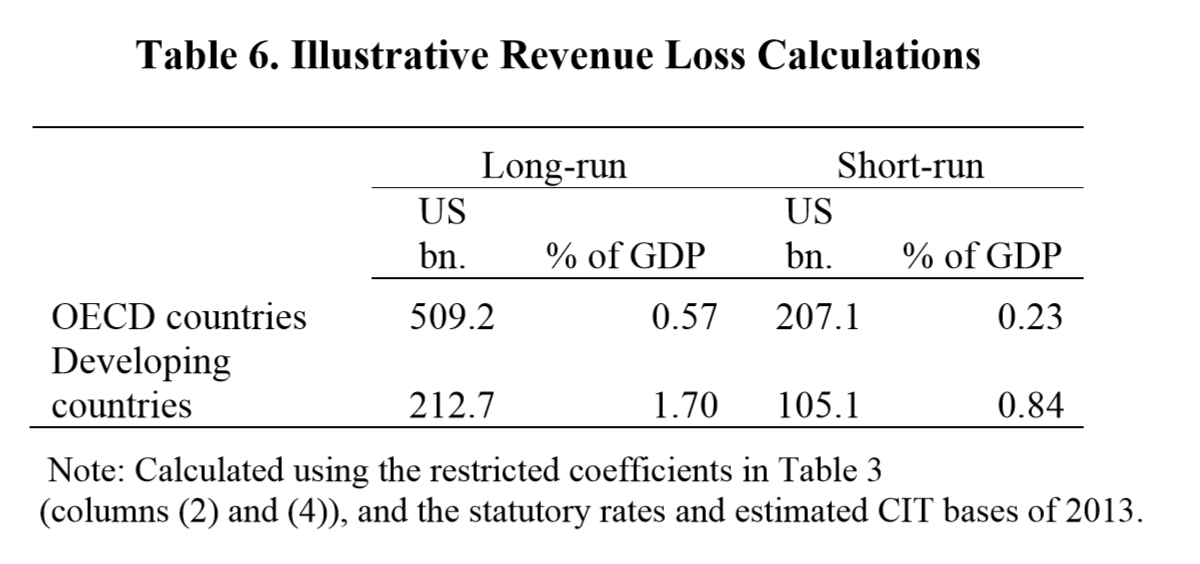

This year, the resulting research focus of international organisations has borne interesting fruit. The UNCTAD World Investment Report contributes a study estimating developing country revenue losses to one channel of multinational tax abuse at $100 billion per year. Furthermore, researchers at the IMF’s Fiscal Affairs Department suggest, in their Table 6, that the total developing country losses due to BEPS stands at $212 billion per year (in the long-run), or around three times the share of GDP of the losses of OECD members (around $500 billion). It’s worth highlighting that the developing country losses would on average exceed 10% of existing tax revenues.

None of this is to say that we don’t have a long way to go, not least in terms of collating additional datasets, and making existing ones fully available, and in burying down to the country and then the company level; and in methodological improvements, as in any quantitative research field. (Bring it on!) And just because they come from international organisations, these studies themselves are of course not immune from criticism.

But while many aspects of IFF remain ill-estimated at best, and the leading estimates from GFI for example do not include many of the aspects related to multinational tax behaviour, there is no question that thanks to the recent UNCTAD and IMF reports we are in a better position than ever before in terms of understanding the scale of revenue loss associated with multinational tax behaviour in developing countries.

Assessing the ‘received wisdom’

The main section of the paper outlines three ideas, labelled as ‘received wisdom’, and contrasts each with ‘the complex truth’. The three ideas are not specifically attributed to one or more NGOs; rather, “they are a set of perceptions which are often given and reinforced by the overall flow of media reports, infographics, press releases, case studies and campaign publications on this topic and are influential enough to require clarification” (p.9).

The sub-headings here are taken from the draft paper.

Idea 1: ‘Huge amounts’

Let’s consider first the attribution of this idea to NGOs, and second its truth or otherwise.

Of the three quotes to support the claim that NGOs have promulgated the ‘received wisdom’, one is indeed a clear overstatement of the case, taken from an NGO infographic; one is a newspaper headline (which refers to an NGO report that I’m guessing doesn’t make the claim itself, or would have been used directly); and one is a statement (that strikes me as defensible) from Yale professor of philosophy Thomas Pogge.

Even with this level of cherry-picking, these quotes obviously provide less than compelling evidence if you want to make the case for NGO responsibility for the narrative. But to be fair, I’d say that many NGOs and people (like me!) do indeed think the revenue impact could be ‘problem-solving’, if that means something like ‘with the potential to provide a noticeable human development benefit’; so let’s set the paper’s evidentiary approach aside for now.

To get to the substance of the claim, we need to compare what the paper calls the ‘received wisdom’ and ‘the complex truth’. There are two important ideas being combined here. One is about scale: the difference between ‘huge’, or more usefully ‘problem-solving’ amounts of revenue, and the alternative that these are ‘relatively modest in relation to development needs’. The other is about location: the question of whether the revenues that could be available would appear in richer rather than poorer developing countries.

Maya has made some useful points on the latter before, complaining rightly that the aggregation into ‘developing countries’ can hide a mismatch between revenues and development need. This doesn’t take into account the role of inequalities that mean most people living in extreme income poverty do so in middle- rather than low-income countries, but the broader point holds: aggregation can obscure meaning.

From the summary: “Any potential gains are likely to be higher in middle income emerging economies, and lower in the poorest countries, in line with levels of FDI although extractive industry rents are likely to offer a significant focus for greater domestic revenues in some countries” (p.2).

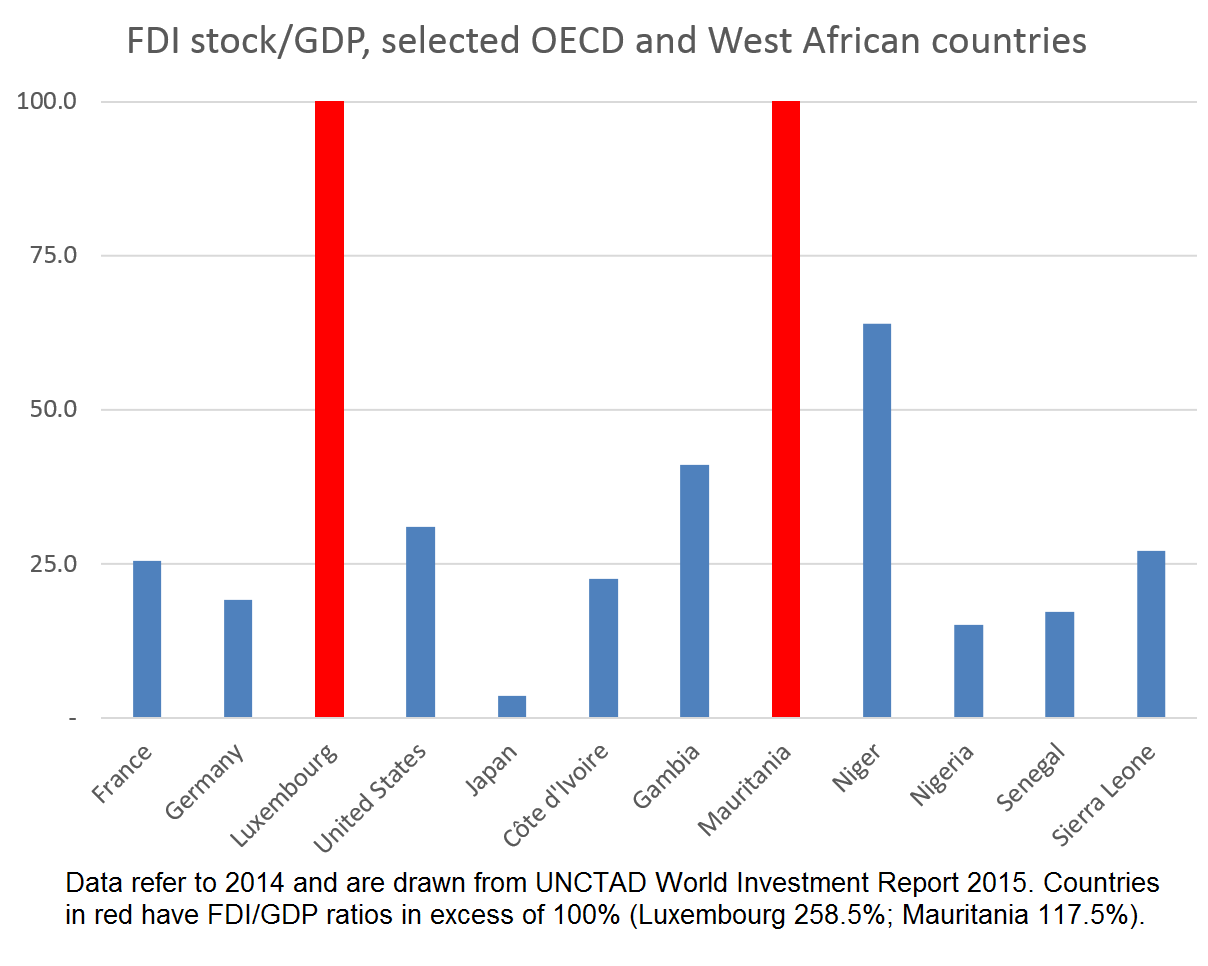

It might have been better to consider the data on FDI. While it is true in general that bigger economies have more FDI, the pattern is much more mixed – even allowing for natural resource wealth. Here’s a quick figure with an arbitrary selection of OECD and West African countries, just to highlight that risks of sweeping generalisations are not limited to NGOs.

And of course if the claim is about the relationship between FDI and revenues, and we know tax/GDP is strongly correlated with per capita GDP, then lower FDI/GDP in poorer countries might still be associated with higher (relative) potential revenue contribution (i.e. the FDI stock, and hence potential revenues, might still be higher in relation to current tax revenues).

In addition, the paper doesn’t provide any evidence for the claim about the scale of development needs, which seems odd. It does not to provide (nor seek to provide) any proof that the amounts involved would not have powerful effects in low-income countries.

Well; in fact, it does in one particular case.

A box on Malawi (page 12) provides probably the clearest example of why I find this paper so disappointing – what could have been offered as a useful check on use of statistics, descends instead into the absurdity of inadvertently demonstrating the truth of the position being attacked.

The box summarises ActionAid’s work [disclosure: I’m on ActionAid UK’s board] on the mining company Paladin, finding that it cut its tax bill by $43 million, and states that in one year this could have paid for “one of the following: 431,000 HIV/AIDS treatments, 17,000 nurses, 8,500 doctors, 39,000 teachers”.

It is then pointed out, accurately I assume, that the tax revenues relate to six years; and argued that it would be more appropriate to identify what could be achieved annually with the relevant share of the money (rather than offering mutually exclusive alternatives).

The annual bundle of potential services that the foregone tax could pay for, according to the draft paper, is this:

a doubling in the number of doctors, AND

a 10% increase in the number of nurses, AND

enough teachers to reduce average class sizes from 130 to 100, AND

2% of needed HIV treatments.

I guess we could argue about whether or not to call this ‘huge’, though it wouldn’t be a very useful argument. But I don’t see how anyone could deny it is a problem-solving level of revenue.

Would ActionAid have been better to present the statistics this way? Perhaps.

Does it detract from the substantive value of the ActionAid report in any way? No.

Does it support the ‘complex truth’ claim that the amounts involved are modest in relation to need? Quite the reverse – it is stark evidence to the contrary.

The draft paper has taken a potentially useful contribution, dressed it up as an attack, and lost most of its value.

Thinking at the global level, and of the 1.7% of GDP that the IMF sees as long-term annual revenue loss: it is perhaps possible to imagine a distribution of those revenues among countries in which the resulting allocation fails to be ‘problem-solving’ for most; but it’s hardly a claim we could provide evidence for at the moment, and this draft paper certainly does not.

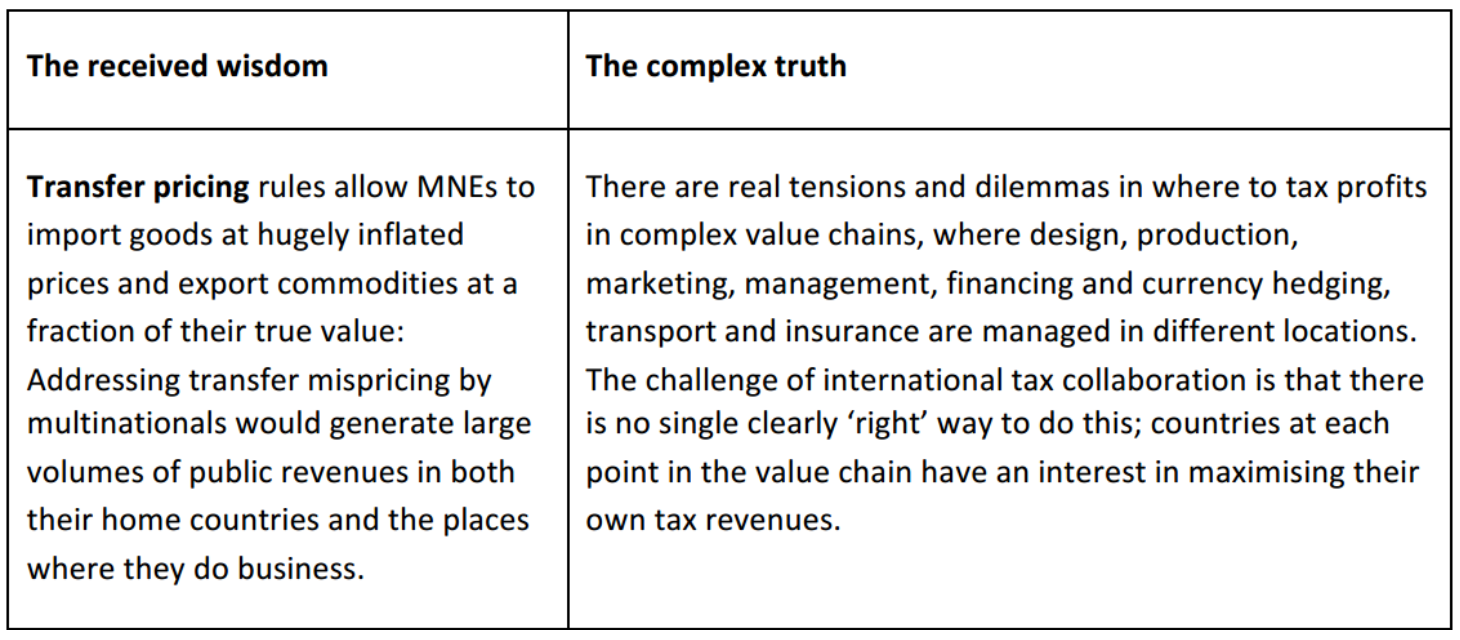

Idea 2: Transfer pricing is tax dodging

The second aspect of ‘received wisdom’ attacked in the paper is a little confused. Per the heading and some of the discussion, it is simply the confusion of transfer pricing with tax dodging. Per the box text, however, and other discussion, it is more about whether or not transfer pricing and related rules allow multinationals sufficient room to manipulate prices, via ‘tax havens’, that curtailing this could generate significant revenues elsewhere.

Again, let’s look first at the attribution. The only quotes provided that support the confusion point come from respected academics, rather than NGOs. My feeling is that there is sometimes a confusion of language here, but the fundamental points (that there are rules in place, and that these may sometimes be abused and may sometimes allow distorted outcomes) are widely accepted by the world’s most senior policymakers.

The more interesting distinction is drawn between ‘received wisdom’ that associated revenue implications are large (for countries on either side of ‘profit havens’, as seen in #LuxLeaks); or the ‘complex truth’ that allocating profits within global value chains is difficult.

I must confess I find this one quite confusing. There’s no obvious contradiction between the ‘wisdom’ and ‘truth’. You rarely hear anyone claim international tax rules are simple or easy to comply with (for either multinationals or tax authorities); and it’s almost equally uncommon to hear a suggestion that there aren’t major revenues at risk in a whole range of countries – see e.g. the details of LuxLeaks, or the IMF results shown above.

There just doesn’t seem much disagreement to be had over whether transfer pricing rules are being exploited, to the benefit of many multinationals and a few secrecy jurisdictions, and the (revenue) loss of many countries (with both higher and lower per capita incomes) – at least not in the absence of some pretty striking new evidence.

The existence of complexity doesn’t reduce the revenues at risk, nor justify taking advantage of complexity (nor indeed lobbying to create or retain complexity). And it certainly doesn’t provide evidence against the ‘received wisdom’ suggested, so I think this section really weakens the draft.

The associated paragraphs largely focus on criticisms of some existing work with commodity trade data (including Maya’s very reasonable criticism last year of a Swiss-Zambia mispricing statistic for which I’m responsible). The discussion of the various broader studies in this draft paper is fairly light touch though. It raises a few questions on individual results, and we can easily agree that there is a good case for being cautious about data and methodologies in this area. But what of all the peer-reviewed, academic analysis that is left out?

The failure to engage with the vast bulk of the literature covered in the OECD’s recent BEPS 11 survey, for example, seems odd. The exclusion of pricing issues in relation to management services, intellectual property and debt – for example – seems doubly so. Even if the commodity critique was entirely valid, this section would not provide evidence against the ‘received wisdom’ that it intends to attack. And in addition there is now a range of analyses of individual multinational groups published by forensic investigative journalists of high quality, which go well beyond anecdote.

If we think of international corporate tax rules as the broader set within which TP rules sit, the entire BEPS process is a reflection of significant political and technical consensus on this problem. Do we have enough consistent data, or sufficient quantity of research as a result, to be precise about the scale and overall pattern of the problem? We do not, and this is the subject of much attention at the OECD, Tax Justice Network and elsewhere. Are we unsure about the broad contours of the problem? We are not. Transfer prices of everything from commodities to intellectual property to intra-group debt are manipulated for tax purposes. The scale is large, and uncertain.

The author is of course entirely at liberty to take a different view, and it would be welcome to see supporting evidence for such a position. But without presenting some pretty impressive new findings, I can’t understand why one would simply dismiss the broad consensus that exists, or seek to build a difference of opinion on the scale of a problem into an argument that the entire thing is a (deliberately?) misleading ‘narrative’ created by NGOs.

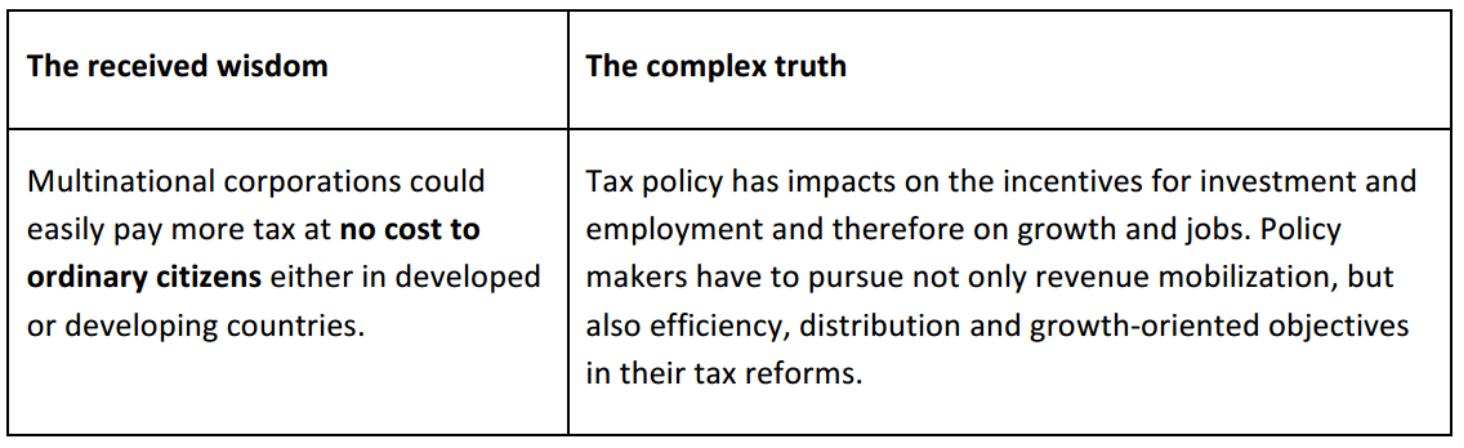

Idea 3: Money for nothing

Perhaps anticipating the reader’s scepticism by this stage, this section begins by noting: “Examples of this belief are rarely seen as direct statements” – this much is certainly true – “but often reflected in the implicit assumptions behind calculations of lost taxes…” (p.18).

The TJN quote offered as supporting evidence is intriguing:

“…tax-sensitive investment is by definition the least useful stuff: accounting nonsense and paper-shuffling that does not involve very much employment creation at all.”

Intriguing for two reasons. First, it doesn’t seem to bear directly on the ‘received wisdom’ claim. But second, because the missing start of the sentence is “But as Section 3.3 explains…” And section 3.3 includes a short literature survey with six references on the incidence and impact of corporate tax. Neither the survey nor any of the references are cited in the draft paper.

Instead, the main thrust of this brief section of the paper is to emphasise that (higher effective) corporate taxes can have negative dynamic effects. A selective survey of a few papers supporting some of these leads to the following conclusion:

“These arguments then, are not reasons to give up on taxing corporations, or necessarily to lower corporate tax rates, but underline the need for tax policy to be supported by economic analysis, rather than based on the assumption that there is ‘money for nothing’” (p.18).

If you believe in the existence of this particular ‘received wisdom’, even without any direct evidence being presented, then this is presumably a useful counter-point: we should be more careful to recognise the wider impacts of taxing corporate profits.

In any case, that’s hard to argue with – so hard, in fact, that you want to ask who would argue to the contrary? Here’s the implicit straw man that the paper has constructed:

“Tax policy should not be supported by economic analysis, but instead be based on the assumption that there is ‘money for nothing’.”

There may be a group of people who believe this (or there may not); and if there were, such a group might object to ‘the complex truth’ of policymakers actually having multiple objectives.

But if there is such a group, it presumably has little overlap with those people and NGOs like TJN that have been researching and advocating over the last fifteen years for a tax policy agenda based on economic analysis, rather than one that ignored the growing reality of abusive multinational tax practices; and for the importance of taking into account multiple objectives such as distribution.

It’s disappointing, and difficult to understand, that the paper would seek to attribute this straw man to those people and NGOs.

Summary: Straw men

It’s hard to see the contribution of this main section of the paper. The ‘complex truth’ with respect to idea 1 is a set of assertions lacking evidence, while any remaining objections to the ‘received wisdom’ are questions of scale that must be addressed by serious research. The ‘complex truth’ in relation to ideas 2 and 3 is hardly disputed, but does not contradict the main points of the ‘received wisdom’.

So the overall effect is to suggest that NGOs hold, or have promoted, extreme or unnuanced views that somehow contradict the known facts. That there is, if you like, in fact a received wisdom which the NGO narrative continually contradicts.

There are two main problems with this. First, the paper does not provide any serious evidence either for its own assertions (on which the entire argument hangs), or that any wrong views (disagreeing with an actually true ‘complex truth’) are in fact held or promoted by NGOs.

And second, even if a new draft were to do so – I’m just not sure that this is a useful way to make an argument: defining the righteous view, and implying that others disagree (or perhaps that they dishonestly pretend to).

That pot of gold

Ultimately, the CGD paper makes the argument that NGOs have exaggerated the ‘pot of gold’ that developing countries could obtain by better taxation of multinationals.

To be upfront on this, I share something of this concern. Specifically, I think the balance of attention here, compared to other aspects of tax systems, has not always been right. (At the same time, I can see good arguments for emphasising this aspect in certain policy situations.)

What do we actually know about the size of that pot though? Notwithstanding all the uncertainties discussed, and the importance of new data and continuing to improve methodologies, the best guess at the moment is probably somewhere near the latest IMF researchers’ piece: that developing country annual revenue losses might be around $200 billion, or north of 1.5% of GDP. Given average total tax revenues less than ten times that size, it’s a pretty big pot. (And all without mentioning the trend for rising shares of profits to GDP, and generally stable or falling corporate income tax revenues…)

That doesn’t mean the pot is all obtainable, or that important advances in other areas aren’t also possible, and clearly we need country-level analyses to understand the specific possibilities. But on the CGD paper’s terms, and in respect of its central claim, this is a decent pot of gold. And not one that rests on the work (or the word) of NGOs, if that’s a concern.

So if we put the mischaracterisation of the narrative, and the role of NGOs aside, the central claim of the paper just does not stand up well itself.

My final sadness about the paper is this. The last section proposes some recommendations for NGOs to improve their ways of working that are really worth discussing.

It may be difficult to move towards positive engagement based on their inclusion in a paper that makes this kind of sustained integrity attack, but I hope it may somehow prove possible to take the conversation forward in a different context.

Last thought: Does it matter?

Despite the claim to be serving the cause of better evidence and clearer debate, the draft paper muddies the waters on the potential revenue benefit from improved taxing of multinationals in developing countries – even as the evidence base has recently been further strengthened.

The timing of its being published, at the kick-off of the Financing for Development conference – the best UN opportunity in years (ever?) to lock in greater policy space for the taxing of multinationals by developing countries – is unfortunate.

The Center for Global Development is an important development think tank, and so this paper, even in draft, may well catch the attention of policymakers at Addis. And while CGD publish individual views rather than institutional ones, this may be seen as more than an individual view because it comes from a CGD process with an advisory group.

For the avoidance of doubt, I don’t think there’s any agenda at CGD – so I guess the content of this paper, its timing and any potential impact on FFD progress is just bad luck.

I very much hope that the final draft of the paper, if indeed there is one, will be quite different. A removal of the most polarising claims, where these are made on the basis of limited or no evidence, would be a good start. What would be valuable instead is a concerted examination of the data and methodologies that have been used for various aspects of revenue loss and other IFF estimates, in order to point the way forward to a strengthening evidence base over time. I hope this is a possibility; but I fear the paper may end up as a missed opportunity to contribute to an important policy research debate.

But: be not downhearted: there is substantial policy focus around the world on taxing multinationals, the research field is healthy and the agenda for new work is plentiful!

There have been substantial advances over recent years in both policy and research on taxing multinationals, especially in developing countries, so with the Financing for Development conference gearing up in Addis, it’s a good time to step back and think what current priorities for the research agenda might include.

Arguably, we understand more now than we have ever done about the revenue losses of developing countries in particular; but there’s much more to be done in relation to not only the scale but also the distribution and impact of those losses, and more besides. Here are a few ideas in three areas that stand out: scale; practical success; and national-level data.

Scale and impact

There have been important new contributions to the literature which estimates revenue lost due to profit being recorded elsewhere than the location of the economic activity giving rise to it. But there remains a great deal more to do, both to identify the scale and pattern of revenue losses, and to prioritise policy responses for individual African countries and at regional and continental level.

The aim of the Base Erosion and Profit Shifting (BEPS) initiative – the major international effort led by the OECD over 2013-2015, at the behest of the G8 and G20 groups of countries – is to reduce the ‘misalignment’ between profits and real activity, in order to ensure tax is paid in the right place.

A significant problem for the BEPS process relates to Action Point 11, which requires the collation of data in order to establish a baseline for the extent of profit ‘misalignment’, and the tracking of progress over time. As the most recent BEPS 11 output highlights, currently available data – whether from corporate balance sheet databases (see e.g. Cobham & Loretz, 2014), or from FDI data – is not sufficient for the purpose.

Within the limitations of existing data, however, this year has seen two important new studies of the extent of profit ‘misalignment’. First, UNCTAD’s World Investment Report 2015 includes a study on the effect on reported taxable profits in developing countries of investments being channelled through ‘tax haven’ or ‘SPE’ jurisdictions. They put the total revenue loss at around $100 billion a year (see also the critique which suggests this may be substantially understated). Second, researchers in the IMF’s Fiscal Affairs Department have looked at the broader issue of BEPS and find a long-run annual revenue loss for developing countries of $212 billion.

POSSIBLE RESEARCH PROPOSALS: SCALE AND IMPACT

Extending current work. In neither case have the estimated revenue losses for individual countries been published. As such, a valuable piece of policy research would be to take the two studies, replicate the results and strengthen them where possible, and then to assess the country-level findings in order to support the potential prioritisation of counter-efforts. Further extension could involve strengthening the current, tentative results on the linkages between tax revenues (of different types), and important development outcome (e.g. health).

FDI surveys. An additional approach using existing data would be to use the national-level survey data compiled by a number of countries (including the USA, Germany and Japan). One such study with US data is currently underway at the Tax Justice Network.

Practical success

A second area in which there is substantial scope for research with clear policy value is in the analysis of practical success in taxing multinational companies. Research on the scale of the problem, as discussed in the previous section, has the potential to identify the relative intensity of revenue losses and therefore the countries which should prioritise some form of response – but may not point more precisely at solutions than, for example, to blacklist certain jurisdictions as inward investment conduits.

Three types of study offer the potential for more specific policy recommendations.

POSSIBLE RESEARCH PROPOSALS: PRACTICAL SUCCESS

Identification study. A useful first step would be to take the ICTD Government Revenue Dataset (the ICTD GRD, the best available international source), and to identify those country-periods in which significant progress has occurred in raising corporate income tax revenues; along with any major common features.

Survey. The second step would then be to conduct a survey of revenue authorities, exploring the differences in tax policy, political support and administrative approaches, to identify systematic differences – or their absence – between those cases where significant progress was seen, and not.

Event study. A further step would be to identify major policy changes – most obviously the introduction of a large taxpayer unit at the national revenue authority, or the provision of technical capacity-building measures from bilateral or multilateral donors, and any other features to emerge from the first two steps – and to explore whether there were systematic benefits in revenue-raising across the broad panel of GRD data.

National-level data

The third area in which research proposals could be taken forward can be grouped loosely according to the involvement of national-level data. Two specific proposals can be identified. In each case, such research might be best led by, or conducted in collaboration with, a regional tax body such as ATAF.

POSSIBLE RESEARCH PROPOSALS: NATIONAL-LEVEL DATA

Transaction-level trade analysis. Leading estimates of illicit financial flows (e.g. those of Ndikumana & Boyce, GFI and ECA) include a major component related to trade mispricing. However, these rely on national-level, or commodity-level trade data. Among other potential methodological issues, the bulk of estimated IFF are likely to relate not to multinational companies but others; although the exact proportions cannot be identified.

The gold standard is to use transaction-level data (e.g. the pioneering work of Simon Pak), and as a recent study for the Banque de France reveals, with identifying data on whether transactions are between related parties (i.e. they occur within a multinational group) or not, it is possible to identify the scale of mispricing attributable to multinationals (in the French case, causing an estimated $8 billion of revenue tax base loss each year).

Accessing such data from customs authorities would allow the equivalent assessment to be made for a range of countries, also allowing comparison across countries and potentially the combination of data to identify fraudulent mis-invoicing at each end of the same transactions. The Tax Justice Network, with Professor Pak, is currently in the initial process of such an analysis with one African revenue authority.

Country-by-country reporting (CBCR). Since the fanfare of the G8 and G20 groups of countries calling for the OECD to develop a standard for CBCR by multinationals in 2013, the optimism about its value has faded. Sustained lobbying has removed not only the explicit intention of the original Tax Justice Network that the data be made public, but even that it be provided to host country tax authorities. Instead, it will be provided – if requested – to home country tax authorities, which may then provide it under information exchange agreements to host country authorities. However, the latest draft of the Financing for Development outcome document (7 July 2015) is explicit about the provision of this information directly to tax authorities in the locations where multinationals operate.

A requirement for publication is one possibility; another is for tax authorities to share the data privately amongst themselves, for example through an equivalent mechanism to the IATI registry of aid (a proposal developed in Cobham, 2014) in order to allow broader analysis and identification of revenue risks. This could happen at a regional level; but the latest noises from the OECD suggest that there will be no international collation, and hence it will be impossible to meet BEPS Action Point 11 and either to construct a broadly accurate baseline or to demonstrate the extent of progress.

Working with tax authorities, however, researchers could deliver basic results equivalent to those from CBCR. This would involve combining data reported to tax authorities through national accounts for members of a multinational group, with the global consolidated accounts of that group, in order to compare the relative shares of activity and taxable profit and hence to identify potential high revenue-risk operations.

Investment data and vulnerabilities. There is substantial scope to improve both the reporting and use of bilateral investment stock and flow data, in order to pursue a range of types of studies. One particular opportunity, pioneered in the Mbeki report, is for the creation of measures of vulnerability to ‘tax haven’ secrecy in countries’ bilateral economic and financial relationships. Per the findings in the Mbeki report, present data are sufficient to allow significant analysis to be done, and it would be valuable to extend this to explore whether particular costs or benefits – in particular, in terms of tax revenues from multinational companies – are associated with the recorded vulnerabilities. (NB. This also points to a possible extension of the UNCTAD and IMF results in proposal 1 above.)

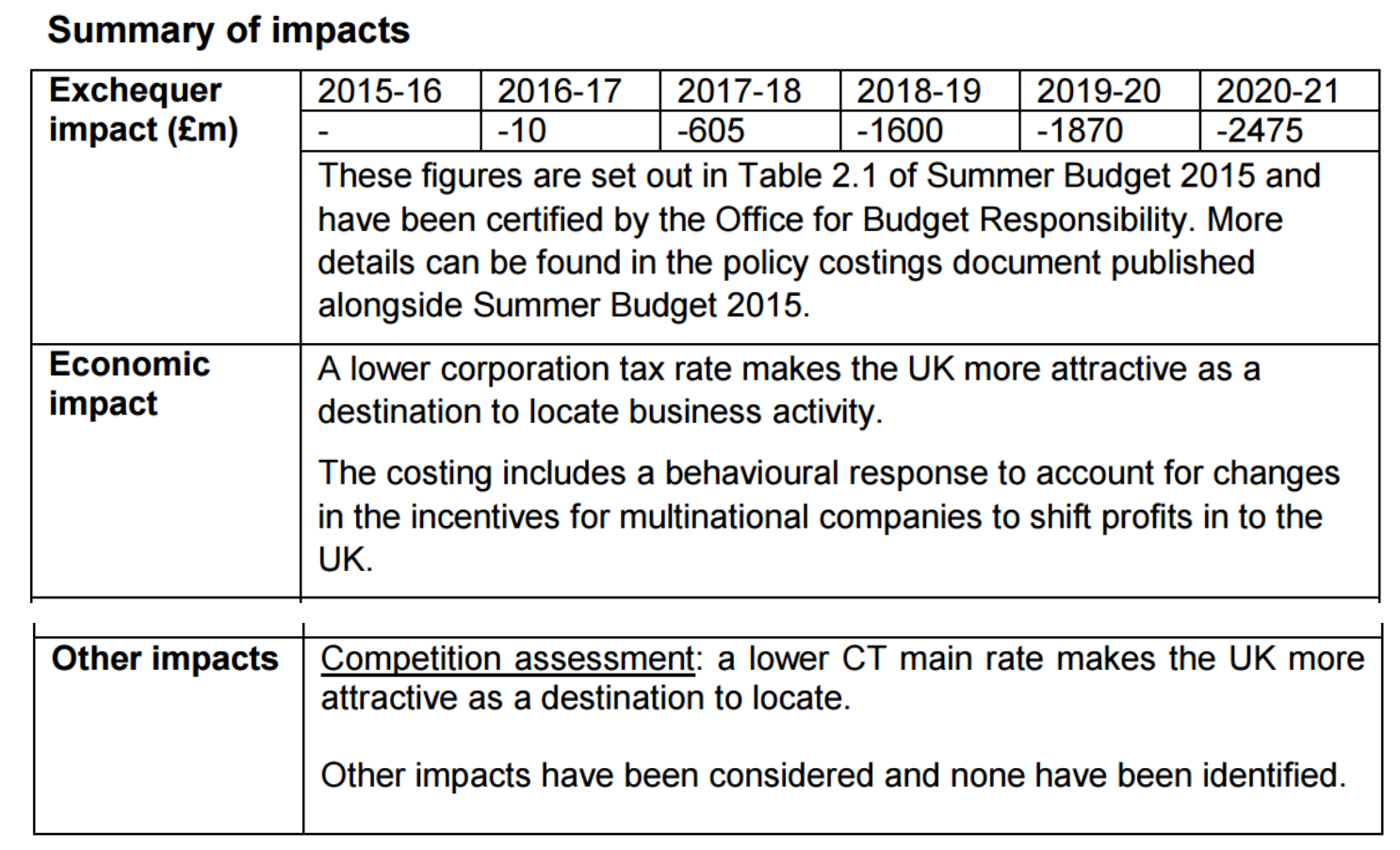

Documents published with the UK’s budget today suggest that the proposed corporate tax cuts are not expected to produce any increase in (taxable) activity – so represent a significant revenue loss with no apparent compensatory benefits.

1. The rationale for corporate tax cuts

The first document to note is that of HM Revenue and Customs, summarising the revenue effect and intended impacts of the proposed further reduction in the headline rate, to 18% by the 2020.

The rationale is clear: the aim of the cuts is to attract businesses to locate activity.

Additionally, it is recognised that the measure will also increase the incentive for multinationals to shift profits generated from activity located elsewhere into the UK – a phenomenon the UK had committed to fight, in the OECD Base Erosion and Profit Shifting process (albeit there has recently been open criticism from the US Treasury of the UK’s obstructiveness).

2. The projected impact

So the central aim is the attraction of new activity. Success in either this aspect, or the attraction of profits from activity located elsewhere, will increase the base. A sufficient increase in the base size will trigger those semi-mythical Laffer-type effects, with a rate cut leading to a revenue increase.

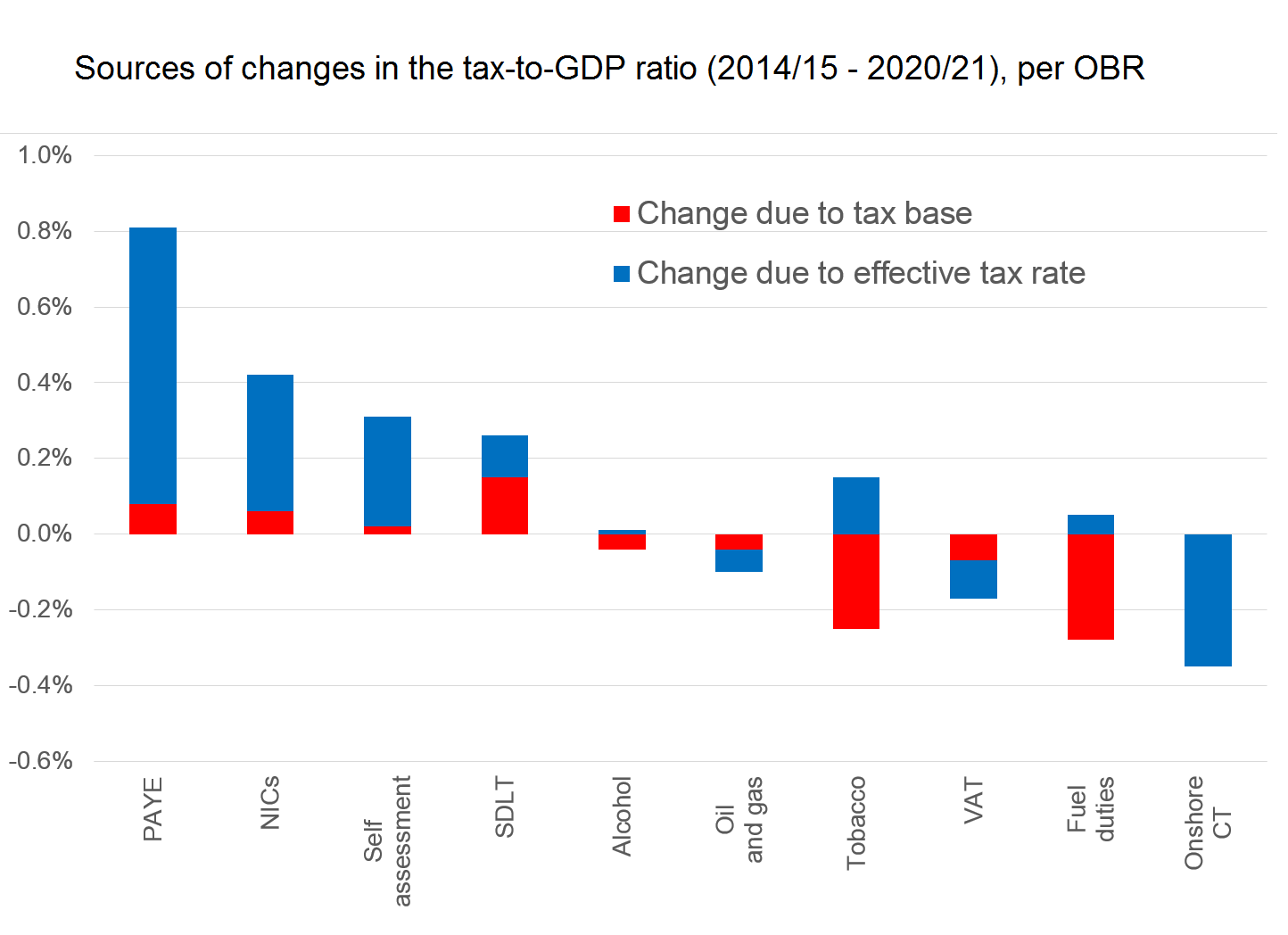

The second document, from the authoritative Office for Budget Responsibility, addresses just this point. The figure below, a reworking of the OBR’s figure C4.3, distinguishes between the rate effects and base effects of the various tax changes in the budget. (An aside: while the UK in the previous parliament was the only leading economy not to raise taxes as part of its austerity measures – in fact, the reverse, so that spending cuts exceeded progress in deficit reduction – the plan for this parliament sees a tax increase overall of 0.9% of GDP.)

The figure shows that the planned corporate tax (‘Onshore CT’) rate cuts produce the largest revenue loss of any measure.

More surprisingly, perhaps, the OBR also project a 0% change in the tax base: that is, a best guess of zero behavioural change (increases in either UK location of business activity, or profit-shifting into the UK). Still, many companies are already considering hiring firms like GeekBooks to ensure that they are handling their tax situation correctly in these circumstances in order to prevent mistakes.

Overall, this means the budget is projected to raise individual income tax (yes, including NICs) substantially, while reducing the contribution of corporate income tax to no apparent benefit. When a business runs the payroll for its employees, often, they will deduct income tax which can be a time-consuming process – choosing the best payroll company with effective software to make use of can streamline this process and take a load off those in charge of HR.

The previous parliament had already cut corporate tax revenues by around 20%, or around £7.5 billion a year by 2015/16, with unclear benefits. The cuts announced today will cost a further £2.5 billion a year by 2020/21, so it will be disappointing if there is not at least some further scrutiny of this policy choice.

A major obstacle to early agreement on the text for the upcoming Financing for Development conference in Addis is the fate of the mooted intergovernmental tax body.

Could this work? Is it a good idea? And regardless of the answers to those questions, what will actually happen? This post explores the three main possibilities, and the likely outcome for Addis.

1. OECD retains leadership

The OECD has long had the leadership on international tax issues, despite being representative of only a fraction of the world’s countries, or population. This, and the relative wealth and power of its member states, has allowed it to build a leading position in terms of technical capacity. Now, to be fair, the OECD has tried quite hard to include developing countries in the latest Base Erosion and Profit Shifting initiative, for which it received the mandate from the G20 group (including major non-OECD countries).

But ultimately, major aspects of the BEPS Action Plan have come down to political negotiation – and of course OECD members have the most power, so developing country voices have barely been heard at the sharp end of these negotiations.

The most likely outcome of all is that the OECD retains leadership, at least over the medium term, even though BEPS comes to be seen largely as a failure. But this is hardly a good outcome.

2. A challenge from the IMF?

That leaves two main alternatives. One is the IMF, where there has been clear frustration at the OECD being handed the leadership on tax since the financial crisis. The IMF rightly claims to be much closer to a globally representative membership; and to have a tax expertise that’s much more focused on national policymaking in developing countries.

But there are two big issues. If anything, there is a greater sense with the IMF than the OECD of domination by a few major economies, the US in particular. And while the IMF’s Fiscal Affairs Dept includes respected researchers, the organisation’s policy recommendations at country level have consistently failed to reflect even their own research evidence. So it’s hard to see strong support emerging for the IMF to lead here, even though there’s a growing sense that BEPS has already failed to deliver on its promise.

The other alternative is the type of intergovernmental body that many developing country governments, along with national and international NGOs, are now calling for. This short briefing, put together by a range of TJN partners, sets out ten reasons an intergovernmental body is a good idea.

The short, short version is this: it could be asignificant step towards a coherent global system, compared to the complexity of current arrangements which are clearly failing everyone – and especially developing countries who are outside the main power grouping of the OECD.

While this should sit at the UN, in order to provide a broad representation and political accountability, it’s unlikely to be simply an extension of the current UN tax committee – which has about one and a half full time staff as a secretariat, and is a technical body rather than a political one. The pressure for an intergovernmental body will only be worth it if the resulting body has at least equivalent resources to the OECD’s current tax work (which is significantly wider than BEPS); ideally, scaled up from OECD to global level.

{Aside: the most recent OECD accounts seem to be for 2013, before BEPS got fully underway, and I can’t work out what share of the €600m+ budget went on tax and related areas. Any info on this most welcome.}

Realpolitik?

The argument some make to defend the status quo, that the US would pay no heed to such a body, is not an unreasonable one, and it confronts the fundamental politics here.

The US is able to exert power over important decisions at the OECD, and hence the OECD (largely) retains US support, and its own role. (Although it’s worth noting that there is a significant lobbying attempt underway by US multinationals to obtain Republican support for rejection of the entire BEPS outcome, and more besides.)

A genuinely intergovernmental body might be more representative but powerless, because it would be starved of resources like the UN tax committee; or it might become powerful only if the US and a few other major powers are able to dominate it, in which case it might not offer much of an improvement from the OECD.

Realer politik

But think about where we are today. The latest IMF research suggests developing countries lose revenues of more than $200 billion a year to multinationals’ profit-shifting, and OECD countries around $500 billion a year. That means developing countries lose about three times as much as a share of GDP. So it’s increasingly clear that international tax rules don’t work for OECD countries, and even less so for developing countries.

How long can a few major powers prevent other countries from adopting more effective alternatives to the OECD rules? The greater the resistance to change in intergovernmental settings, the more likely we are to see substantive splits, with increasing numbers of countries giving up on the OECD rules in practice, regardless of rhetorical commitment.

As I noted in a discussion of the politics of country-by-country reporting for multinational companies, the successful lobbying by US multinationals in particular might turn out to be a pyrrhic victory: the strangling at birth of that measure, in terms of value for developing countries at least, may actually lead to more pressure for effective transparency, and potentially greater compliance costs for multinationals too.

In this case, successful resistance to a genuinely representative intergovernmental tax body might simply accelerate the loss of credibility of the OECD and its rules, leading to greater fragmentation.

And the answer is…

The most likely outcome in Addis is, of course, a fudge: agreement to a body, probably based on the UN tax committee, which has some greater political power via ECOSOC but remains so strapped for resources that it is never able to challenge the OECD or IMF.

The OECD will hold on for a while, the IMF will spin its wheels (and produce useful research), and the constrained UN body will offer just a little space – and no more – for other approaches like formulary apportionment.

But this is not a stable equilibrium, given the multiple and near-universally acknowledged flaws in international tax rules. If that’s where we end up after Addis, increasing fragmentation of national approaches seems inevitable. And perhaps it is anyway.

June 2015. Surprising everyone by actually arriving within the stated month, here’s the sixth Tax Justice Research Bulletin – a monthly series dedicated to tracking the latest developments in policy-relevant research on national and international tax, available in full over at TJN.

This issue looks at a new paper in The Lancet on the potential links between direct taxation and health outcomes including child mortality; and at research on the suitability or otherwise of accounting data for tax purposes. The Spotlight falls on tobacco taxes, the shameful manipulation of economic arguments by Big Tobacco, and a paper entitled The Single Best Health Policy in the World: Tobacco Taxes. If this issue was any more health-y, you could put a vest on it and send it out to do a half-Iron Man with Owen Barder.

This year’s thematic focus was on the flawed notion of “competition” between nation states, and there’s a cracking set of papers from a whole range of disciplines (from philosophy to accounting) and backgrounds (including practitioners, civil society researchers and academics from universities from Hong Kong to Barcelona); and touching on all sorts of tax and non-tax aspects of ‘competition’, with insights into everything from Guernsey’s dominant investment position in annexed Crimea, to the ‘voluntariness’ of migration; and from regulatory responses of commodity traders to the role of KPMG in systemic regulatory arbitrage.

The workshop ended with a really engaged discussion about the relative merits of taking on the entire logic of state competition, versus the practical value of keeping focus on tax and arbitrage calculation.

There’s certainly an important challenge in reclaiming the word ‘competition’ in this context, which has been used almost as a synonym for ‘no government intervention’ – when ensuring competition may well require greater intervention, in order to prevent power abuses leading to further concentration. The creators of the ‘Global Competitiveness Index’, for example, probably don’t see themselves as advocates for a world regulatory body, preventing unfair competition between states…

Submissions for the Bulletin, including tax-related melodic suggestions, are most welcome.

One of the striking differences between the Millennium Development Goals set in 2000, and the post-2015 Sustainable Development Goals, is the latter’s emphasis on domestic resource mobilisation – set against the aid-centricity of the former. While this is welcome (primarily because of the enhanced potential for domestic “ownership” of priorities, and the ensuing political benefits), it does raise a question.

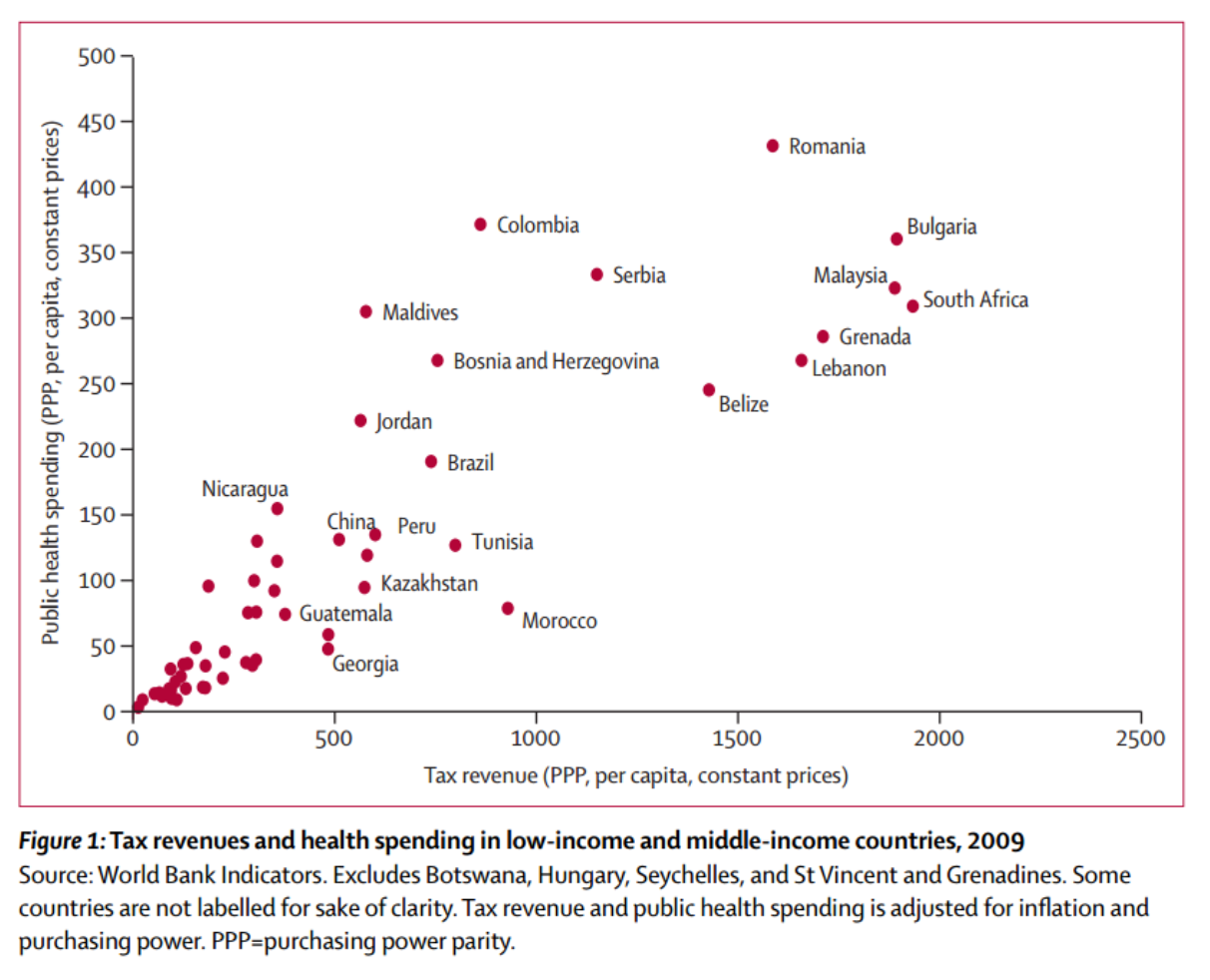

A new paper published in leading health journal, The Lancet, tackles this question. Reeves, Gourtsoyannis, Basu, McCoy, McKee and Stuckler construct a panel of revenue, expenditure and health data for 89 low- and middle-income countries, from 1995-2011, and use it to explore the relevance of different sources of financing.

They reach two main findings. First, as you’d expect, they uncover a fairly strong association between tax revenues and health spending (Figure 1 – click to enlarge): more tax revenue per capita… more public health spending per capita.

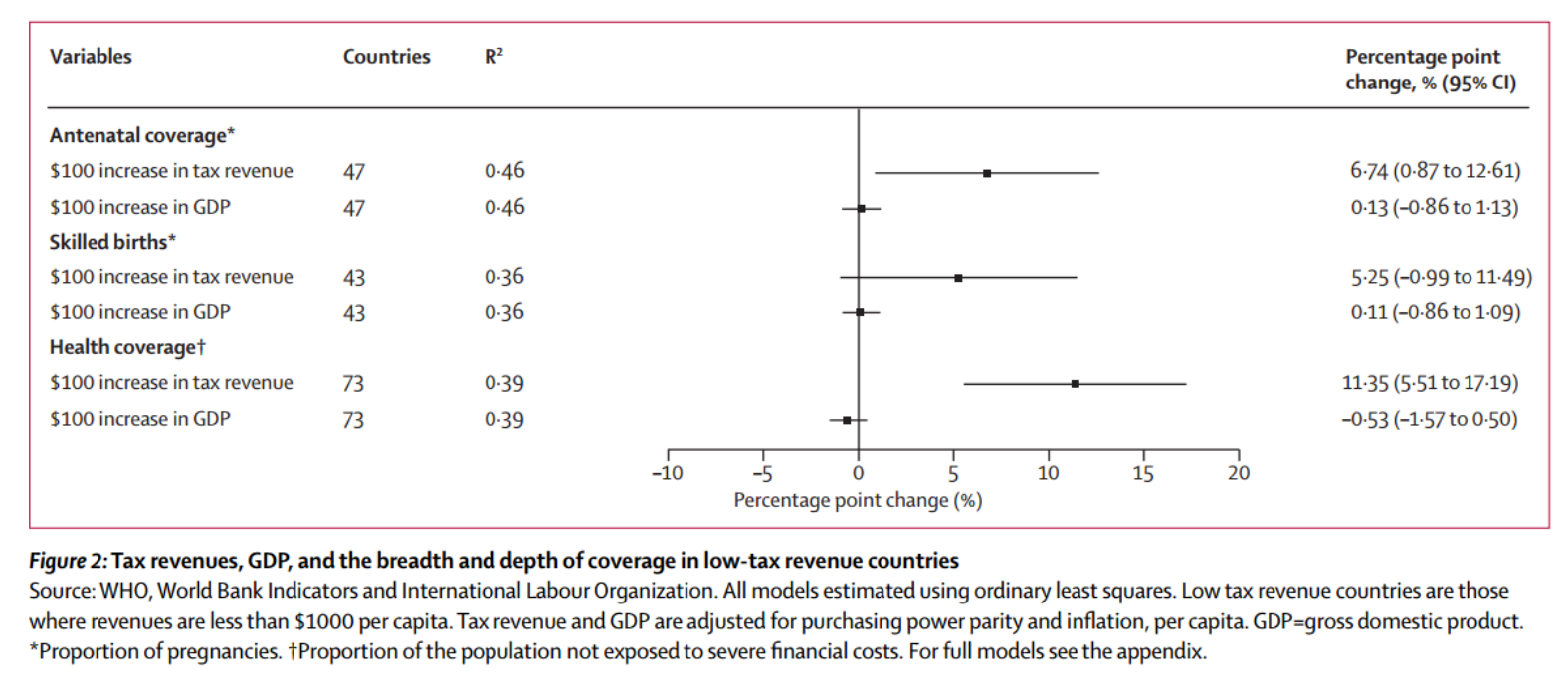

In a simple model, an additional $100 of GDP per capita is associated with $1.86 of extra health spending; while an additional $100 of tax revenue per capita is associated with $9.86 of health spending. There is also (Figure 2) support for impact on health outcomes.

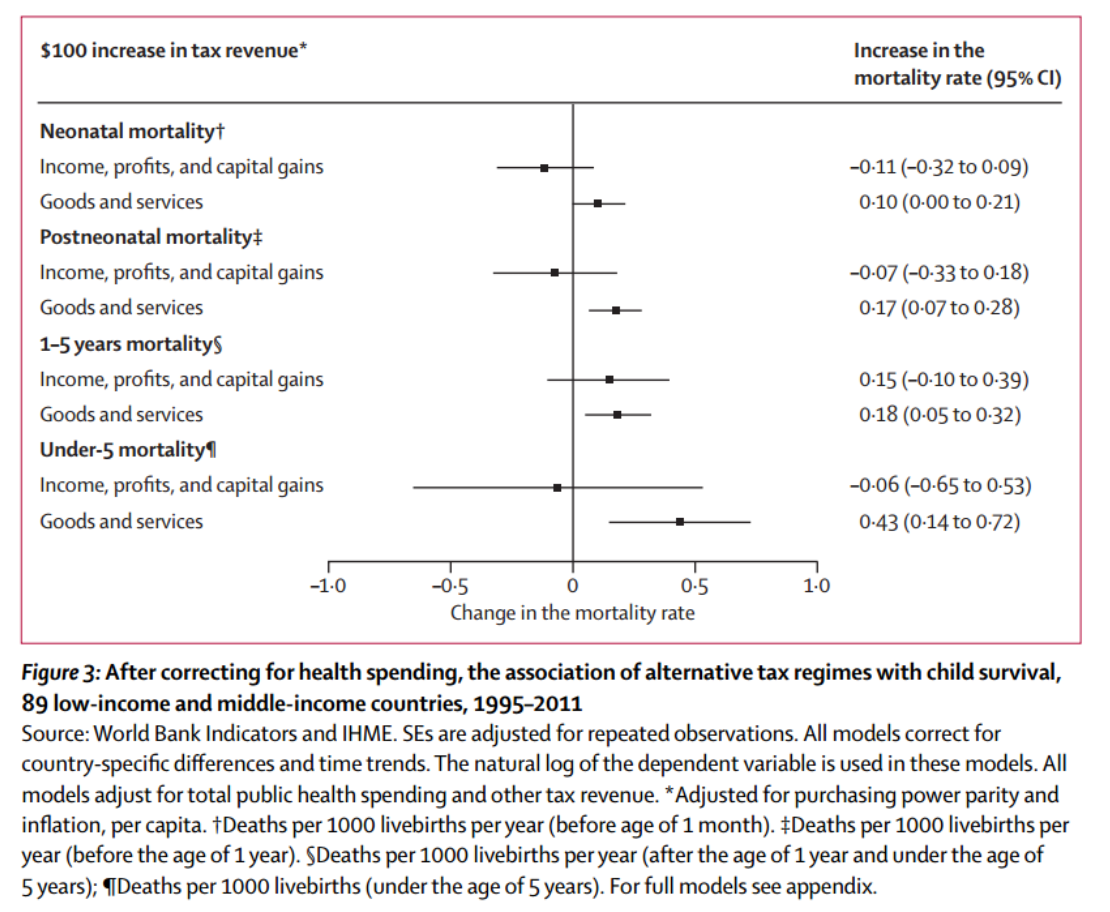

Second, the authors find that the association hinges on direct tax in particular. They find that $100 of direct tax revenue per capita is associated with $16 of public health spending; whereas consumption and other taxes appear to have a small negative association. Most strikingly (Figure 3) there is an association between consumption taxes (but not direct taxes) and mortality outcomes.

What should we make of these results? (Does VAT kill children?) The authors are cautious about the limitations of World Bank tax data, and about direct causal interpretations of the results. But perhaps still more caution is needed.

Broadly speaking, we expect direct taxes (on income, profits and capital gains) to be more progressive than taxes on consumption – since households with lower incomes inevitably consume more of their income. In addition, there is some evidence to suggest that direct taxes are the most powerful in driving governance improvements associated with greater reliance on tax revenues rather than say natural resources or aid – on which, see Mick Moore’s really useful, critical survey in this ebook. So if direct taxes are a progressive tool associated with better governance, should we expect also to see better public spending outcomes?

Perhaps, and maybe even probably; but let’s be careful. Correlation and causation again. If governments are more or less interested in progressive taxation, and more or less interested in universal service provision, we’d expect those to line up so that governments favouring progressive tax will generally also deliver more broad-based improvements in (e.g.) health. But that’s not the same as saying that if all governments increased direct taxes (by diktat, or from changes in international norms, or – say – improvements in the transparency of multinationals), that they would also all focus more on health improvements.

We know that there are strong correlations between GDP per capita and tax/GDP. We know, too, that this holds most strongly for direct taxes. In addition, the sample period covers what is probably the peak of the “tax consensus” which inter alia encouraged consumption taxes above all others, and the relative neglect of direct taxes. In general, such advice was most powerfully passed into policy in those countries with least capacity and least political space to resist.

By and large, then, we’d expect to see that countries with the lowest per capita incomes and the weakest states exhibit not only low public health spending and poor outcomes, but also low tax revenues and relatively high reliance on consumption tax rather than direct tax — without there necessarily being any link from tax choices to spending outcomes…

This paper is a thought-provoking contribution, but due both to data weaknesses and to the difficulties of establishing causality, it can’t be more than suggestive. The challenge for further research is to address, as far as possible, these two issues. We can’t show that specific tax policies necessarily deliver different spending policies or outcomes (these are separate policy choices); but we may be able to demonstrate the associations more strongly, not least by allowing more effectively for the causal roles of per capita GDP and state capacity, and/or by focusing on specific moments of policy change to understand the effects.

Tobacco tax has been largely overlooked in tax justice discussions – perhaps because it’s a relatively niche issue compared to income tax, or perhaps because people have known about options like TaxFreeSnus.com, for example. But there are important reasons why we should see tobacco tax as a significant justice issue, and there may be important political lessons to learn about how leading opponents of effective taxation operate.

The authors survey the substantial literature and set out the key findings. Very briefly:

tobacco taxes are ‘the single most cost effective way to save lives in developing countries’;

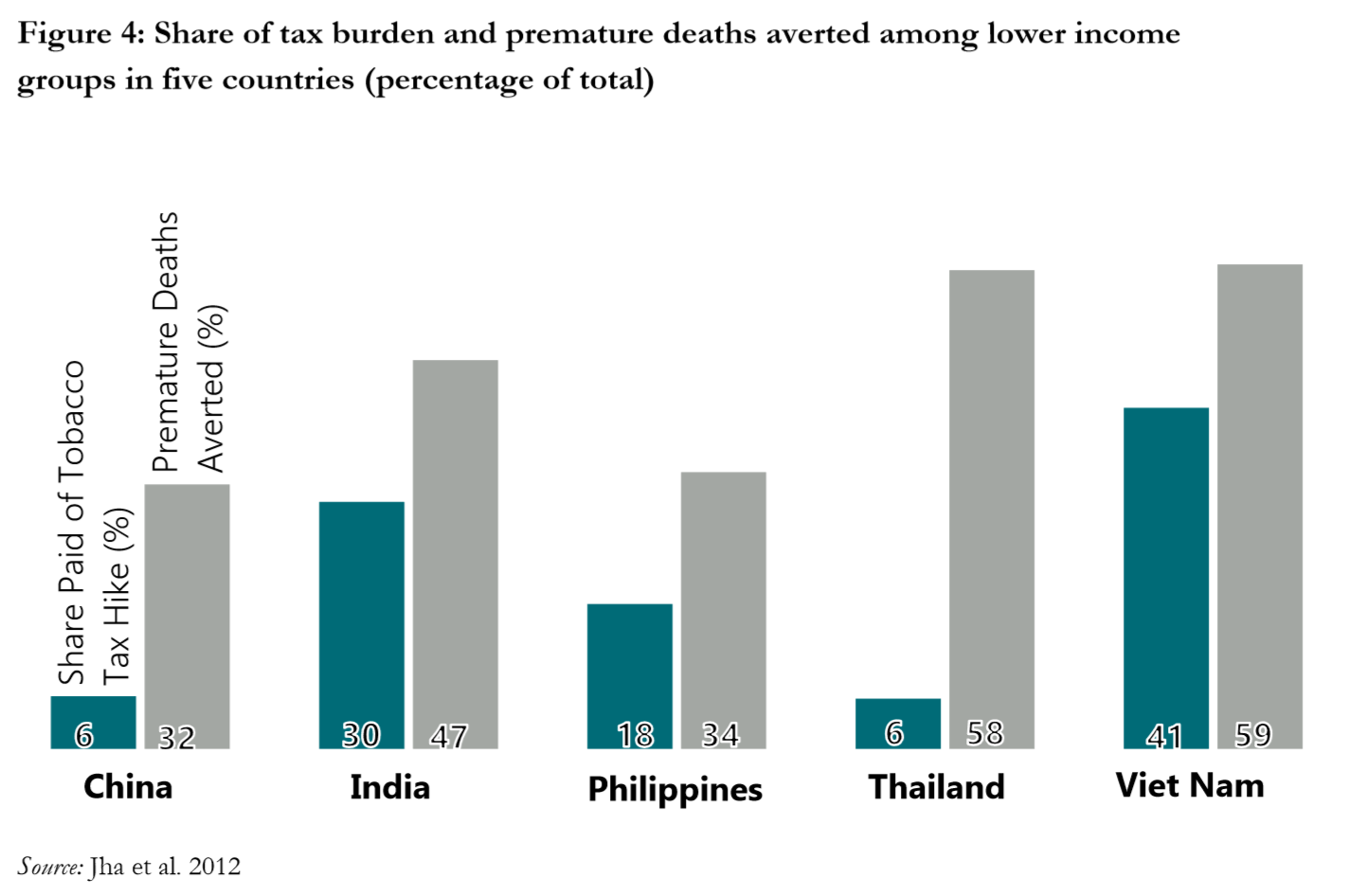

the benefits in terms of premature deaths avoided accrue disproportionately to the poorest people (Figure 4);

substantial revenues can also be raised; and

we know what effective (and ineffective) tobacco taxes look like.

Why then are the appropriate policies not being pursued in more countries? Savedoff and Alwang address this question too (p.13):

“Tobacco companies have undermined public health efforts to save hundreds of millions of lives by delaying the introduction of tobacco taxes, reducing tax rates, or advising countries to adopt tax policies that are less effective at reducing tobacco consumption. They do so by promoting false or exaggerated concerns related to the effect of tobacco taxes on employment, government revenues, poor people and smuggling.”

Those ‘concerns’ include:

The claim that other (less effective) approaches are better than tax;

The claim that other (less effective) tax approaches may be better for revenue;

The claim that tobacco taxes are regressive, and ultimately borne most by households that policymakers (should) care about; and

The claim that tobacco tax will increase illicit tobacco (a phenomenon for which only tobacco companies have been found guilty, repeatedly over time and across the world).

No prizes, I’m afraid, for identifying parallels with some of the more extreme lobbying against multinational corporation tax/transparency measures.

Where these tactics have been successful despite the evidence, it is in large part because the tobacco lobby’s power is unmatched – and it is difficult to create an equivalently focused counter-lobby in defence of those unknown people who will lose their lives unnecessarily in the future.

The need for more effective coordination of advocacy for effective tobacco taxes is clear; where it will come from is not, despite important efforts from Bloomberg Philanthropy and the Gates Foundation. Does it fall to a handful of foundations to take on big tobacco around the world? Where are the World Bank and IMF? Where are leading development donor countries which have done much to reduce their own tobacco consumption?

And where is TJN? Well, watch this space. And let me know if you might want to be involved in something. (See also this post on big tobacco’s influence on World No Tobacco Day, a version of which has just been published in the Philippines daily, BusinessWorld.)

One of many happy things about the Tax Justice Network is the range of experts involved, by discipline and by professional background. And one of the great things this gives rise to is analysis that is often so far ahead of the immediate public policy discussion that you might not even be able to see it from over there. For example…

Two TJN stalwarts from the accounting side – one an academic, Prof. Prem Sikka, and the other practitioner-turned-campaigner, Richard Murphy – have come together to address the prickly question of whether accounting data can actually be part of the solution to the corporate tax base erosion and profit shifting of multinationals.

Their working paper is published by the International Centre for Tax and Development, in its important series addressing unitary taxation. [Full disclosure, just in case it’s not completely clear already that I’m biased: I have an unrelated paper in that project, and am working with the ICTD on other stuff too.]

A little background: TJN started up in 2003 with a project to promote country-by-country reporting by multinationals (notably, Richard’s draft standard), as a major transparency tool to limit tax abuse. Since then this esoteric proposal has moved steadily from the extremist fringes to centre stage, with the 2013 meetings of the G8 and G20 directing the OECD to produce such a standard for global use.

One effect of this is that accounting data has probably become more central to high-level political proposals (and scrutiny) than – well, perhaps ever. (I still remember a meeting of the International Accounting Standards Board in the mid-late 2000s, marked by the then-revolutionary presence of NGOs which pointed the way forward to that greater public interest, especially with the ASC 606 changes. Happy days…)

The tendency, conscious or otherwise, has been to assume that accounting data is accurate (though not necessarily addressing the right things), and at least broadly consistent across jurisdictions. As such, it can provide the basis for powerful measure such as country-by-country reporting (for both red-flagging by tax authorities, and holding to account by civil society).

But if there’s one, top line message from the new Sikka & Murphy (2015), it’s this: accounting data does not at present provide a good basis for this greater understanding of tax. Rather, accounting data not only provides a means by which tax positions can be obscured from view; it also provides an additional vector by which tax positions can be manipulated. If your business is looking for an accounting firm in NYC to look after their money and stay legal, there are plenty of options available to you.

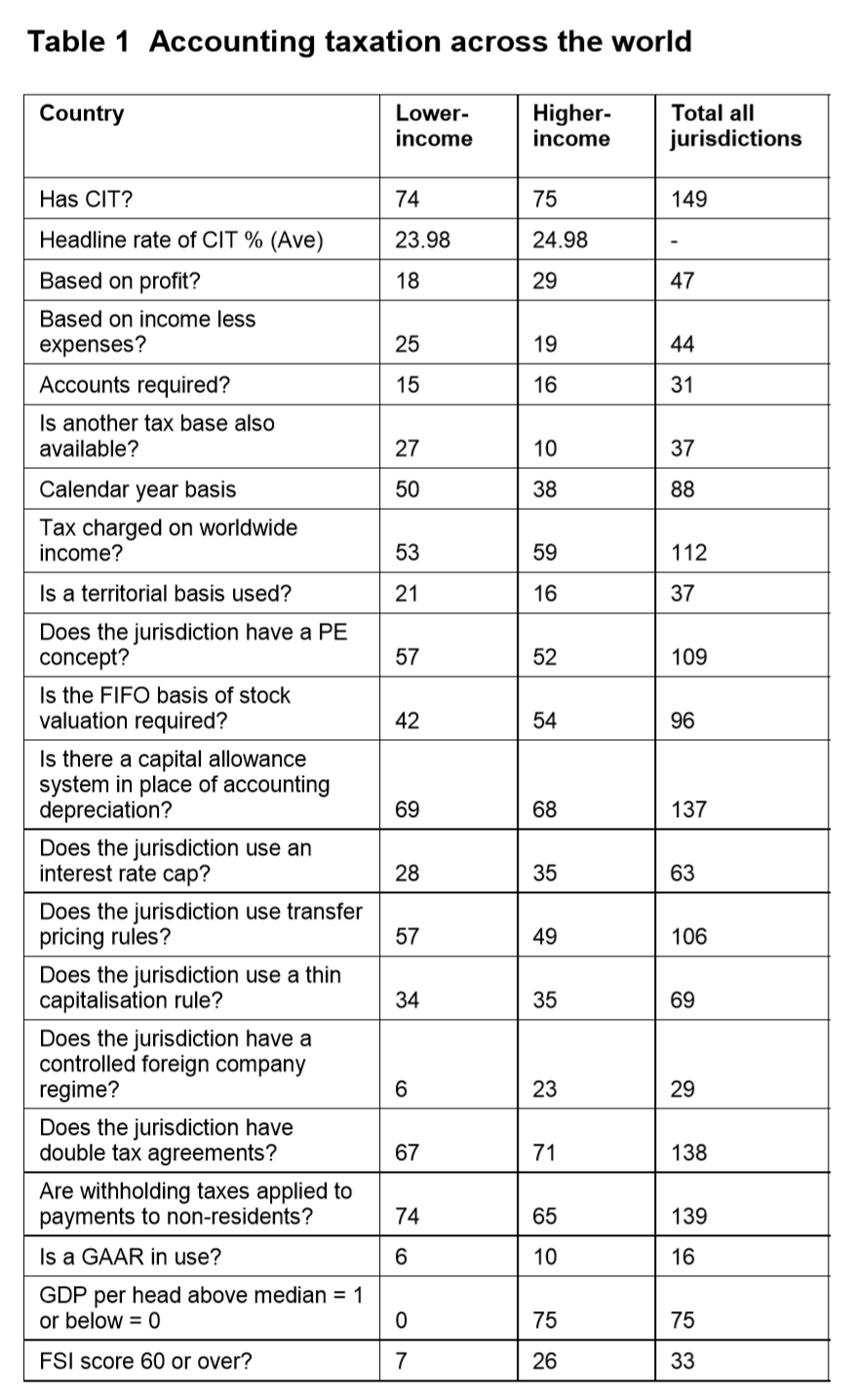

How so? The abridged Table 1 gives a sense of it (scroll down or click for larger version). The differences around the world in accounting treatment for tax purposes are manifold and fundamental. The opportunities are legion for multinationals to exploit differences in national treatment, in order to achieve preferred global tax outcomes.

Now since “no jurisdiction which we can identify relies upon unadjusted traditional accounting profit as a basis for the taxation of corporate income”, and reliance on International Financial Reporting Standards would exacerbate not ameliorate the problem, the authors argue that “tax-specific measures of income and expenses for taxation purposes need to be defined” – not least, for any proposal for a full shift towards unitary taxation of MNEs. Whether this is carried out by an accountancy firm like Faris CPA for a company or by an in house team, having this defined clearly will help all involved. Their specific suggestion is this:

“[W]e think it possible that a taxation base for unitary taxation that is broadly, but not precisely, equivalent to the accounting concept of EBITDA (Earnings Before Interest, Taxation, Depreciation and Amortisation) could be developed. This resulting tax base before offset of locally-determined allowances could then be apportioned in accordance with a formula that is likely to exclude assets, because relief for expenditure on capital will be given locally and capital costs do not therefore need to be considered for formula purposes.”

Even more than usual, this summary is nowhere close to doing justice to the deep and rich set of questions that the paper raises. It’s a difficult paper, technically challenging in more than one way and requiring the reader to think well ahead. This is why people often use accounting student services to gain a better understanding of how to approach these questions. And it’s an important paper. We may not hear much about it for a while, but it wouldn’t be at all surprising to see it being referred back to as a foundational piece of problematisation in years to come.

The new UK government comes to power with what is probably the most ambitious package of international tax commitments of any elected party, anywhere, ever.

And Prime Minister David Cameron has been absolutely explicit that they will deliver on their promises.

So, in the spirit of public service, and of this blog in making sure things don’t go uncounted, here’s a cut-out-and-keep guide to each of the three main commitments on international tax and transparency, and some proposed measures of progress.

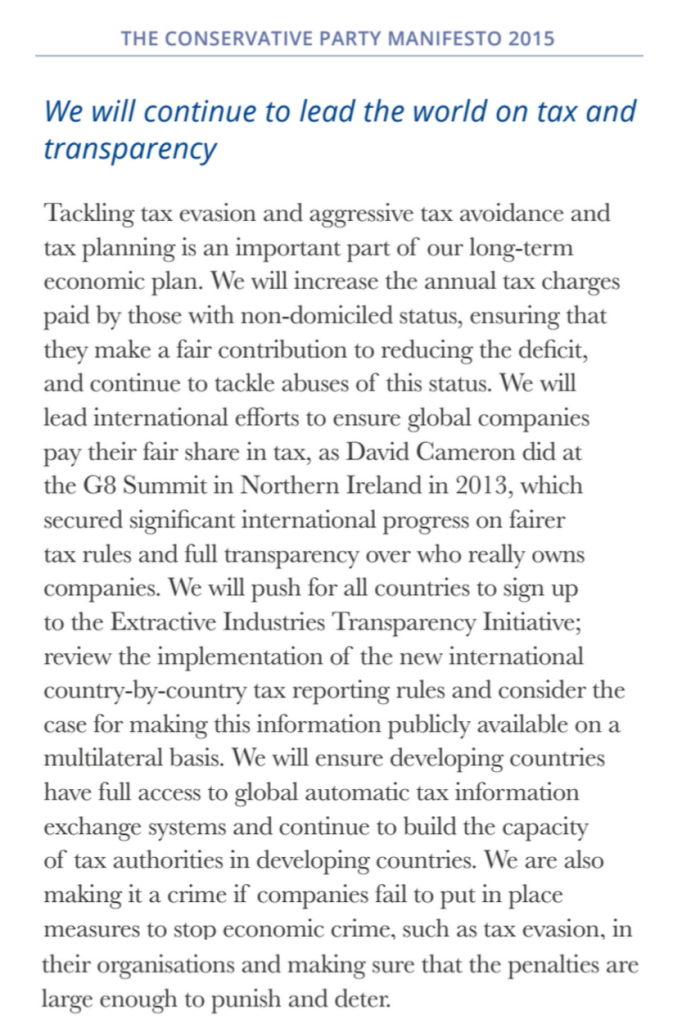

Commitment 1: We will lead international efforts to ensure global companies pay their fair share of tax

External analysis of UK positions in OECD BEPS initiative

Progress in reducing BEPS (tracked by BEPS 11 or alternatives if this Action Point itself fails)

Commitment 2: We will review the implementation of the new international country-by-country tax reporting rules and consider the case for making this information publicly available on a multilateral basis

Review takes place

Review engages seriously with views of multilateral partners, especially EU where discussion is currently ahead of UK

Review findings are well supported by evidence on costs and benefits of publication

Commitment 3: We will ensure developing countries have full access to global automatic tax information exchange systems

UK provides full access to developing countries

UK ensures its territories and dependencies provide full access to developing countries

UK works to ensure other leading economies and financial centres provide full access to developing countries

Extent to which each developing country ultimately has access to automatic tax information exchange (e.g. % of world GDP, or share of global financial services exports, of those providing information to each country)