On the subject of incidence, we each made competing claims about the evidence, as you’d expect. To add a little light to the heat, here’s a TJN round-up of economic research findings on this important question; and some interesting points raised from a different perspective by David Quentin.

There’s been a good deal of coverage of the European Commission decision that Belgium’s ‘excess profit’ tax scheme is illegal, and so it must claw back unpaid tax from companies that were able to achieve double non-taxation on profits shifted into the jurisdiction. The focus has largely been on the implications for specific companies. It’s worth thinking more about different jurisdictions involved, and the possible risks facing the big 4 audit firms.

Basis of the EC tax ruling: Guaranteed double non-taxation

First, the ruling seems pretty clear cut, in principle at least, because the ‘excess profit’ approach is so transparently designed to engineer double non-taxation. Much like Ireland’s bad Apple agreement which accepted that the jurisdiction was not entitled to a share of profits that were shifted in but resulted from activity elsewhere, the Belgium scheme determined that any ‘excess profits’ would be exempt from tax.

The scheme defined excess profits as those bigger than an equivalent, purely domestic business would report – in other words, the result of a multinational’s activity elsewhere. Since these were by definition being reported in Belgium and not elsewhere, double non-taxation was the aim and indeed the guaranteed result. Bingo!

Whereas other cases (e.g. LuxLeaks) involved tailored responses to individual companies, the Belgium approach was consistent leading the Commission to conclude simply that:

We did not have to investigate the specific tax rulings to each company that are based on the scheme. They are automatically illegal.

Why Belgium? Who else?

As I said in various interviews, ‘België is niet de grote vis’ (Belgium is not the big fish), and the ruling is fascinating more because of the potential scale if a similar demand for clawbacks were applied to the bigger EU players in the profit-poaching business.

Our study of US multinationals, which we find to shift 25-30% of their global profits, shows that the majority of shifted profit goes through six jurisdictions: outside the EU Bermuda, Singapore and Switzerland; and inside, Ireland, Luxembourg and Netherlands. [New work from the US Joint Committee on Taxation, with access to firm-level rather than aggregate data, puts Cayman ahead of Singapore in the top six; ut the EU jurisdictions remain central.] Using global balance sheet data (predominantly capturing European multinationals), our earlier study confirmed the same three EU jurisdictions and also highlighted the roles of Belgium and Austria.

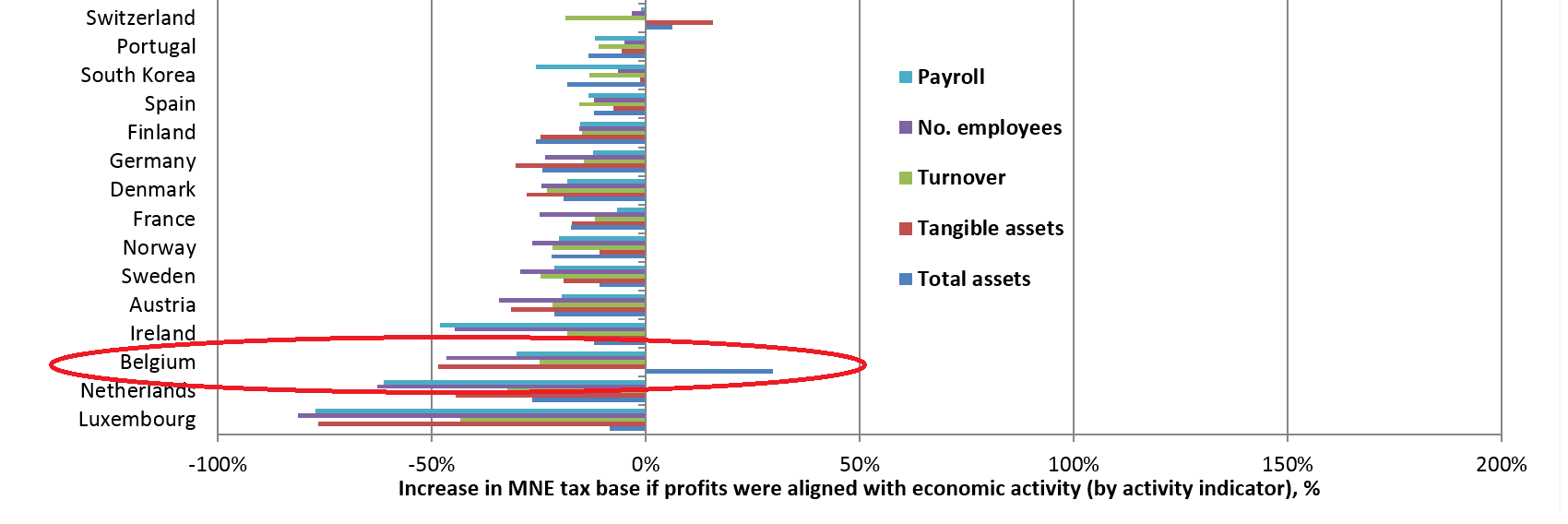

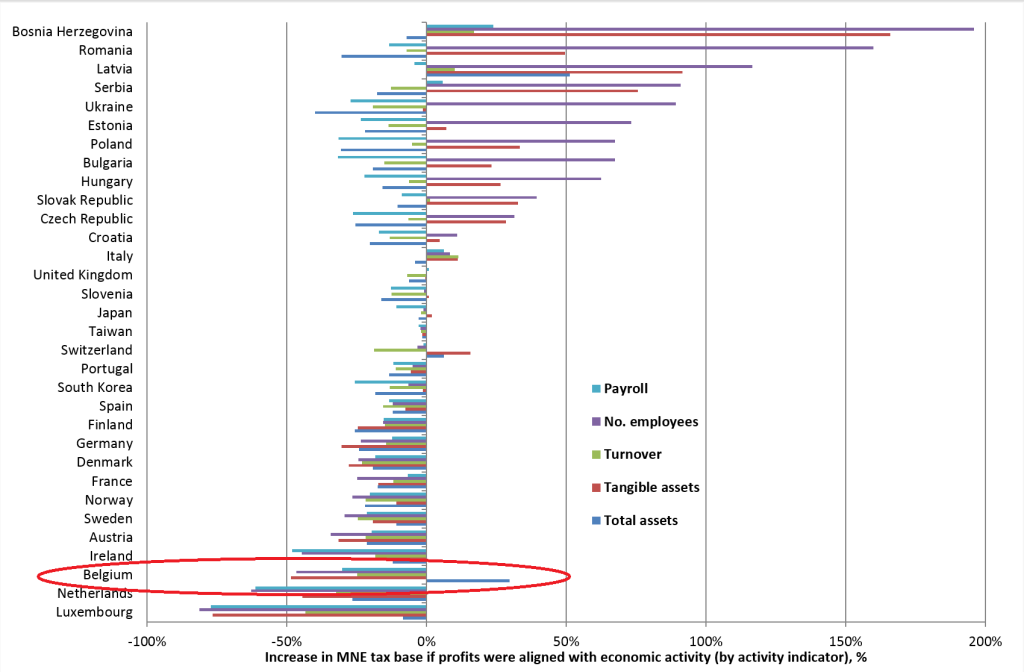

The figure, drawing from the results of Cobham & Loretz, 2014 using Orbis data, shows the share of declared profit which would be stripped away from each jurisdiction, if profits were to be aligned with each of the measures of multinationals’ economic activity (which was the declared aim of the OECD BEPS initiative). Belgium would stand to lose 25-50% of its declared profits under any measure of activity except intangible assets, a relatively extreme position.

Consistent with this view of Belgium as a location for profit-shifting by European multinationals in particular, the European Commission states that the clawback will amount to €700m, of which the bulk – around €500m – relates to European multinationals.

So while Belgium may not be such a grote vis internationally – it doesn’t register for US multinationals in the aggregate, for example – it’s certainly big enough for the European Commission to have bothered with.

But the really big money would be at stake if the same type of decision were to be taken with respect to the profit-shifting into Ireland, Luxembourg and the Netherlands. Of these, the relative complexity of mechanisms in the Netherlands (using trusts and special purpose entities for example, rather than blunt rulings) may make it a harder target. But rulings in Ireland and Luxembourg are already in the Commission’s sights. If the doubly non-taxed profits here were required to be retrospectively taxed at applicable statutory rates, the effects would be substantial indeed.

Company calculations

What would that look like from the point of view of companies involved? Consider the Belgian case. Gross profit that might have faced an effective rate of 15-20%, say, in the countries where the underlying economic activity took place, was shifted into Belgium and declared as ‘excess’ and therefore not subject to tax – in any jurisdiction.

Applying the unmitigated Belgian statutory rate instead will have two main results. First, the overall tax paid will almost certainly (assuming interest is dealt with appropriately) be higher than if neither the scheme itself, nor any alternate profit-shifting arrangement, had been used. The Commission notes that for the Belgian companies used, 50-90% of profits were ruled as ‘excess’; so it’s unsurprising that companies like AB InBev are assessing their options.

The second effect is a more forward-looking one: the changes that the Commission decision may imply for current and future profit-shifting strategies. If the possibility exists for retrospective taxation on shifted profits, do companies become less aggressive? Or is there simply a premium put on the more complex and/or iron-clad methods – for example, will Netherlands structures become even more dominant? Will it favour the UK’s CFC and patent box mechanisms, now with the OECD BEPS mark of acceptability, over other (smaller) jurisdictions?

Big 4 risks

A further impact is that on the big 4 and other professional services firms that may have provided the advice on which basis multinationals made the particular profit-shifting decisions – and themselves profited substantially in doing so. If there is a case for companies to sue over bad advice in the Belgian case, imagine the exposure – for example – of PwC, if a substantial share of LuxLeaks cases were equivalently unwound? If so then at some point, given the vast scale of profit-shifting and the potential tax liability if statutory rates rather than 0-1% were to be applied, a question of financial viability could even arise.

Looking forward again, will multinationals approach such tax advice differently if the possibility of retrospective action remains? Does this simply reduce the value of the advice, or change the willingness to consider it?

And for the big 4 and their staff, with the nature – and some of the risks – of selling profit–shifting advice now impossible to ignore, what are the ethical considerations?

An opportunity for Belgium?

Finally, what can Belgium do? Not such a big fish perhaps, but definitely on the hook. The immediate upside is unexpected tax revenue; the downsides are many.

First, the country stands clearly exposed for antisocial behaviour: profit-poaching in a time of austerity, when the social costs of lost revenues in EU partner countries could not be clearer. Second, trust: how will business view the jurisdiction after this reverse? And third, the stability of the model: given the substantial share of profit booked in the country that appears to have been unwarranted, what are the tax implications of losing the right to tax the non-‘excess’ element?

Here’s the opportunity. The one-off revenues from forcible clawbacks should be sufficient to cover for some time the losses from reduced inward profit-shifting. The question is whether Belgium aims to retain a role in profit-shifting – if it tries to appeal the ruling, struggles to regain credibility with multinationals, introduces and promotes new (OECD- and EC-compliant) mechanisms… or if instead, it takes the opportunity of being ‘caught’, and decides to chart a path towards less anti-social fiscal behaviour.

This could, for example, involve taking a lead in pushing for greater transparency of tax rulings; and in advocating for full enactment of the proposed Common Consolidated Corporate Tax Base (CCCTB) and associated proposal for formulary apportionment within the EU, which would eliminate much of the current profit-shifting; and of course publishing country-by-country reporting of multinationals, which would make the extent and direction of it transparent.

A draft paper by Maya Forstater, circulated by the Center for Global Development in time for the Financing for Development conference in Addis, attacks the integrity of many people and NGOs working on tax justice and illicit financial flows.

The claims include:

that (some?) NGOs have “contributed to unrealistic public expectations and an appetite for an overly simplistic narrative about a corporate tax ‘pot of gold’” (p.31);

that (some?) NGOs tolerate “exaggerated interpretations and misunderstandings”(p.33);

that (some?) NGOs do not “engage honestly with debates over economic trade offs [sic]” (p.33); and

that this behaviour is comparable to “the use of exploitative and prejudiced imagery in charity appeals” (p.34).

Blimey.

This is a (really) long post, as I’ll try to cover the breadth and strength of Maya’s many claims. I should say that I took part in the first of two meetings of the group CGD convened to look at the issues. This was really quite a constructive coming together of different viewpoints. But I stood down when the subsequent blog post seemed to ignore most of the common ground and reiterated some earlier attacks on NGOs instead, making some claims about ‘inconvenient truths’ that resurface here. Comparing back, I’m afraid it seems as if the results of the research exercise were pre-determined.

Some main points from the discussion below:

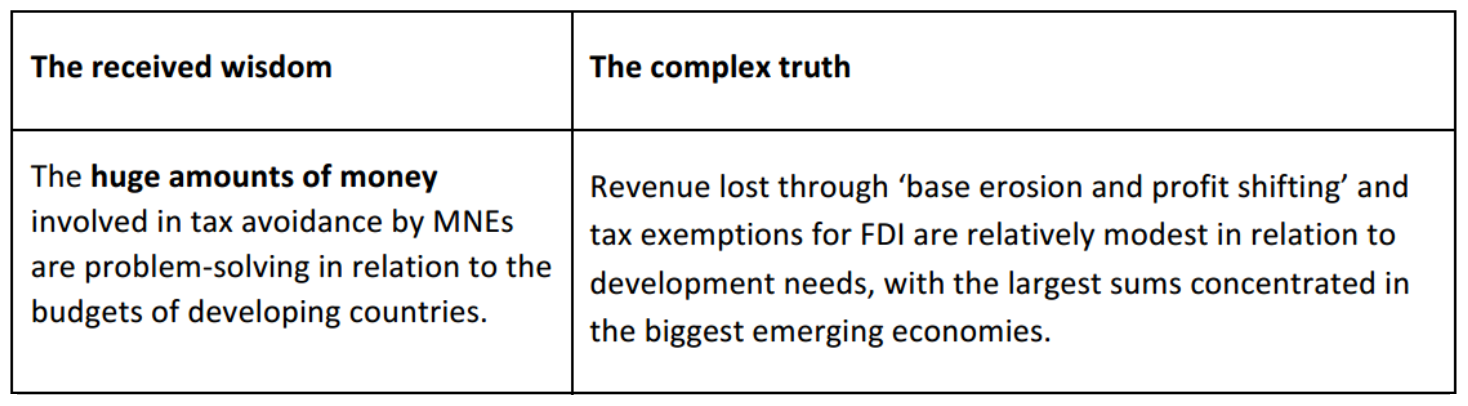

The draft paper makes a series of claims without providing any serious evidence: most importantly, a ‘complex truth’ that tax losses are not of ‘problem-solving’ scale but ‘relatively modest in relation to development needs’. The existing evidence, e.g. from the IMF or – strikingly! – the author’s own analysis in this paper of ActionAid’s work, clearly supports the opposing view.

In the two other cases where ‘received wisdom’ associated with NGOs is contrasted with ‘the complex truth’, there is in fact no direct contradiction – but the presentation in each case creates an implicit straw man of NGO opposition to the truth.

The paper’s main thrust is that there is no ‘pot of gold’ for developing countries – but no substantial evidence is offered to support this assertion. (I’m sympathetic to the idea that this aspect of the tax justice agenda is sometimes overstated, but simply to deny the existing evidence offers no way forward. Indeed this is why I encouraged this work to focus instead on substantive research issues, albeit to no avail.)

I should point out that I was a research fellow at CGD during 2013-2014, and remain grateful to Owen Barder and colleagues for giving me a great deal of space to pursue research in just this area. I hope it may be possible to revise the final draft in such a way that it can make a useful contribution.

Measuring the illicit

The bulk of the attack in the draft paper is dedicated to three elements of ‘received wisdom’, each of which are contrasted with a quite different ‘complex truth’, so I’ll focus on these before coming back to the overarching claims. First, a little bit of context.

As has often been remarked, attempts to estimate illicit financial flows (IFF) are inevitably fraught with difficulty.

By definition, illicit flows are those ‘forbidden by law, rule or custom’: so whether or not they are technically legal, like large-scale tax avoidance, they are always hidden from view where possible. Add to this the fact that the relevant international datasets are often of less than ideal quality and coverage, or sometimes simply held in private by multilateral organisations who should know better, and the problem is of estimating things that are deliberately hidden, on the basis of anomalies in data that are imperfect in any case.

The development of the research field – which has come into being seriously only in the last 15 years – has been led by NGOs, perhaps because academic researchers felt uncomfortable with the degree of uncertainty, or because those at international organisations didn’t see it as a policy priority. At each stage, NGOs and the few academic researchers have challenged international organisations to use their capacity, and ability to access data, to do better; but until this year, there had been no serious response on any aspect of IFF except that of UNODC and the World Bank in their Stolen Assets Recover (StAR) initiative.

Eurodad’s famous 2009 Illicit Financial Flows report, summarising the research contribution of international organisations

Following the G20 meetings in 2009, however, the issues originally promoted by NGOs in the wilderness rocketed to the top of the global agenda. Then in 2013, the G8 and G20 commissioned the OECD to carry out the Base Erosion and Profit Shifting initiative (BEPS), aimed at reducing the misalignment between the location of multinational companies’ economic activity, and where they declare taxable profits.

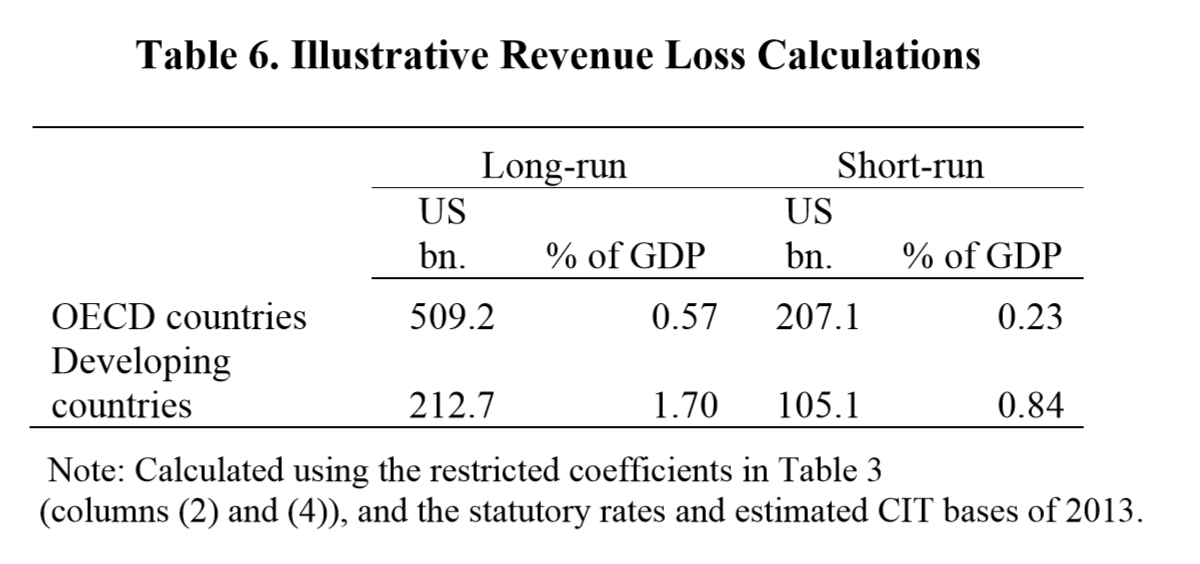

This year, the resulting research focus of international organisations has borne interesting fruit. The UNCTAD World Investment Report contributes a study estimating developing country revenue losses to one channel of multinational tax abuse at $100 billion per year. Furthermore, researchers at the IMF’s Fiscal Affairs Department suggest, in their Table 6, that the total developing country losses due to BEPS stands at $212 billion per year (in the long-run), or around three times the share of GDP of the losses of OECD members (around $500 billion). It’s worth highlighting that the developing country losses would on average exceed 10% of existing tax revenues.

None of this is to say that we don’t have a long way to go, not least in terms of collating additional datasets, and making existing ones fully available, and in burying down to the country and then the company level; and in methodological improvements, as in any quantitative research field. (Bring it on!) And just because they come from international organisations, these studies themselves are of course not immune from criticism.

But while many aspects of IFF remain ill-estimated at best, and the leading estimates from GFI for example do not include many of the aspects related to multinational tax behaviour, there is no question that thanks to the recent UNCTAD and IMF reports we are in a better position than ever before in terms of understanding the scale of revenue loss associated with multinational tax behaviour in developing countries.

Assessing the ‘received wisdom’

The main section of the paper outlines three ideas, labelled as ‘received wisdom’, and contrasts each with ‘the complex truth’. The three ideas are not specifically attributed to one or more NGOs; rather, “they are a set of perceptions which are often given and reinforced by the overall flow of media reports, infographics, press releases, case studies and campaign publications on this topic and are influential enough to require clarification” (p.9).

The sub-headings here are taken from the draft paper.

Idea 1: ‘Huge amounts’

Let’s consider first the attribution of this idea to NGOs, and second its truth or otherwise.

Of the three quotes to support the claim that NGOs have promulgated the ‘received wisdom’, one is indeed a clear overstatement of the case, taken from an NGO infographic; one is a newspaper headline (which refers to an NGO report that I’m guessing doesn’t make the claim itself, or would have been used directly); and one is a statement (that strikes me as defensible) from Yale professor of philosophy Thomas Pogge.

Even with this level of cherry-picking, these quotes obviously provide less than compelling evidence if you want to make the case for NGO responsibility for the narrative. But to be fair, I’d say that many NGOs and people (like me!) do indeed think the revenue impact could be ‘problem-solving’, if that means something like ‘with the potential to provide a noticeable human development benefit’; so let’s set the paper’s evidentiary approach aside for now.

To get to the substance of the claim, we need to compare what the paper calls the ‘received wisdom’ and ‘the complex truth’. There are two important ideas being combined here. One is about scale: the difference between ‘huge’, or more usefully ‘problem-solving’ amounts of revenue, and the alternative that these are ‘relatively modest in relation to development needs’. The other is about location: the question of whether the revenues that could be available would appear in richer rather than poorer developing countries.

Maya has made some useful points on the latter before, complaining rightly that the aggregation into ‘developing countries’ can hide a mismatch between revenues and development need. This doesn’t take into account the role of inequalities that mean most people living in extreme income poverty do so in middle- rather than low-income countries, but the broader point holds: aggregation can obscure meaning.

From the summary: “Any potential gains are likely to be higher in middle income emerging economies, and lower in the poorest countries, in line with levels of FDI although extractive industry rents are likely to offer a significant focus for greater domestic revenues in some countries” (p.2).

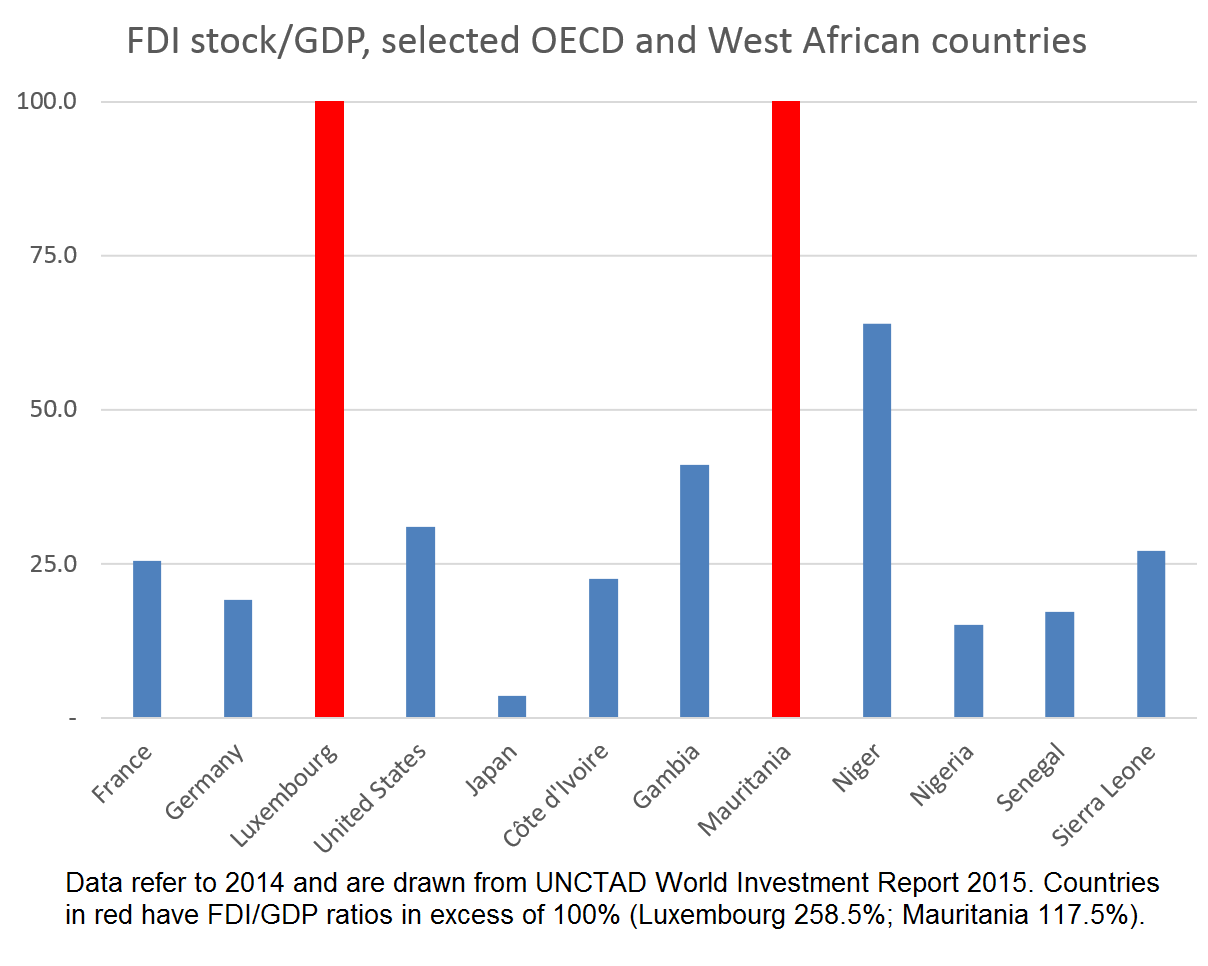

It might have been better to consider the data on FDI. While it is true in general that bigger economies have more FDI, the pattern is much more mixed – even allowing for natural resource wealth. Here’s a quick figure with an arbitrary selection of OECD and West African countries, just to highlight that risks of sweeping generalisations are not limited to NGOs.

And of course if the claim is about the relationship between FDI and revenues, and we know tax/GDP is strongly correlated with per capita GDP, then lower FDI/GDP in poorer countries might still be associated with higher (relative) potential revenue contribution (i.e. the FDI stock, and hence potential revenues, might still be higher in relation to current tax revenues).

In addition, the paper doesn’t provide any evidence for the claim about the scale of development needs, which seems odd. It does not to provide (nor seek to provide) any proof that the amounts involved would not have powerful effects in low-income countries.

Well; in fact, it does in one particular case.

A box on Malawi (page 12) provides probably the clearest example of why I find this paper so disappointing – what could have been offered as a useful check on use of statistics, descends instead into the absurdity of inadvertently demonstrating the truth of the position being attacked.

The box summarises ActionAid’s work [disclosure: I’m on ActionAid UK’s board] on the mining company Paladin, finding that it cut its tax bill by $43 million, and states that in one year this could have paid for “one of the following: 431,000 HIV/AIDS treatments, 17,000 nurses, 8,500 doctors, 39,000 teachers”.

It is then pointed out, accurately I assume, that the tax revenues relate to six years; and argued that it would be more appropriate to identify what could be achieved annually with the relevant share of the money (rather than offering mutually exclusive alternatives).

The annual bundle of potential services that the foregone tax could pay for, according to the draft paper, is this:

a doubling in the number of doctors, AND

a 10% increase in the number of nurses, AND

enough teachers to reduce average class sizes from 130 to 100, AND

2% of needed HIV treatments.

I guess we could argue about whether or not to call this ‘huge’, though it wouldn’t be a very useful argument. But I don’t see how anyone could deny it is a problem-solving level of revenue.

Would ActionAid have been better to present the statistics this way? Perhaps.

Does it detract from the substantive value of the ActionAid report in any way? No.

Does it support the ‘complex truth’ claim that the amounts involved are modest in relation to need? Quite the reverse – it is stark evidence to the contrary.

The draft paper has taken a potentially useful contribution, dressed it up as an attack, and lost most of its value.

Thinking at the global level, and of the 1.7% of GDP that the IMF sees as long-term annual revenue loss: it is perhaps possible to imagine a distribution of those revenues among countries in which the resulting allocation fails to be ‘problem-solving’ for most; but it’s hardly a claim we could provide evidence for at the moment, and this draft paper certainly does not.

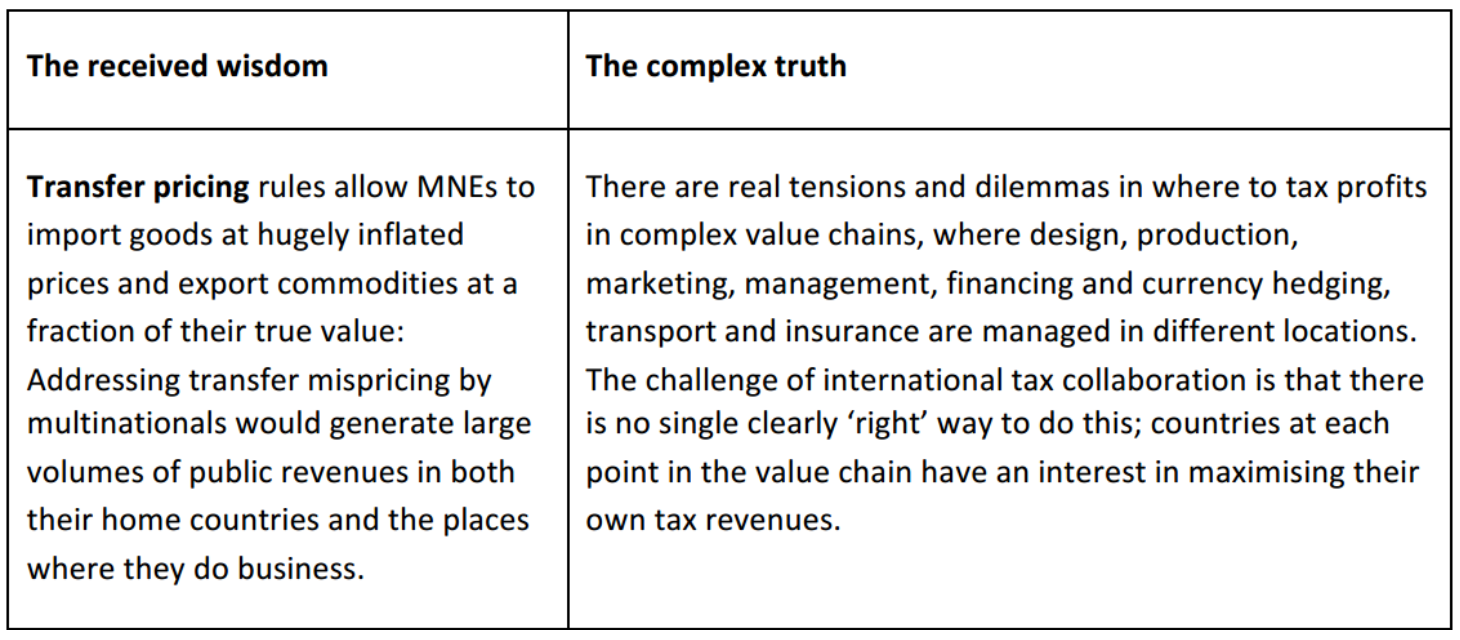

Idea 2: Transfer pricing is tax dodging

The second aspect of ‘received wisdom’ attacked in the paper is a little confused. Per the heading and some of the discussion, it is simply the confusion of transfer pricing with tax dodging. Per the box text, however, and other discussion, it is more about whether or not transfer pricing and related rules allow multinationals sufficient room to manipulate prices, via ‘tax havens’, that curtailing this could generate significant revenues elsewhere.

Again, let’s look first at the attribution. The only quotes provided that support the confusion point come from respected academics, rather than NGOs. My feeling is that there is sometimes a confusion of language here, but the fundamental points (that there are rules in place, and that these may sometimes be abused and may sometimes allow distorted outcomes) are widely accepted by the world’s most senior policymakers.

The more interesting distinction is drawn between ‘received wisdom’ that associated revenue implications are large (for countries on either side of ‘profit havens’, as seen in #LuxLeaks); or the ‘complex truth’ that allocating profits within global value chains is difficult.

I must confess I find this one quite confusing. There’s no obvious contradiction between the ‘wisdom’ and ‘truth’. You rarely hear anyone claim international tax rules are simple or easy to comply with (for either multinationals or tax authorities); and it’s almost equally uncommon to hear a suggestion that there aren’t major revenues at risk in a whole range of countries – see e.g. the details of LuxLeaks, or the IMF results shown above.

There just doesn’t seem much disagreement to be had over whether transfer pricing rules are being exploited, to the benefit of many multinationals and a few secrecy jurisdictions, and the (revenue) loss of many countries (with both higher and lower per capita incomes) – at least not in the absence of some pretty striking new evidence.

The existence of complexity doesn’t reduce the revenues at risk, nor justify taking advantage of complexity (nor indeed lobbying to create or retain complexity). And it certainly doesn’t provide evidence against the ‘received wisdom’ suggested, so I think this section really weakens the draft.

The associated paragraphs largely focus on criticisms of some existing work with commodity trade data (including Maya’s very reasonable criticism last year of a Swiss-Zambia mispricing statistic for which I’m responsible). The discussion of the various broader studies in this draft paper is fairly light touch though. It raises a few questions on individual results, and we can easily agree that there is a good case for being cautious about data and methodologies in this area. But what of all the peer-reviewed, academic analysis that is left out?

The failure to engage with the vast bulk of the literature covered in the OECD’s recent BEPS 11 survey, for example, seems odd. The exclusion of pricing issues in relation to management services, intellectual property and debt – for example – seems doubly so. Even if the commodity critique was entirely valid, this section would not provide evidence against the ‘received wisdom’ that it intends to attack. And in addition there is now a range of analyses of individual multinational groups published by forensic investigative journalists of high quality, which go well beyond anecdote.

If we think of international corporate tax rules as the broader set within which TP rules sit, the entire BEPS process is a reflection of significant political and technical consensus on this problem. Do we have enough consistent data, or sufficient quantity of research as a result, to be precise about the scale and overall pattern of the problem? We do not, and this is the subject of much attention at the OECD, Tax Justice Network and elsewhere. Are we unsure about the broad contours of the problem? We are not. Transfer prices of everything from commodities to intellectual property to intra-group debt are manipulated for tax purposes. The scale is large, and uncertain.

The author is of course entirely at liberty to take a different view, and it would be welcome to see supporting evidence for such a position. But without presenting some pretty impressive new findings, I can’t understand why one would simply dismiss the broad consensus that exists, or seek to build a difference of opinion on the scale of a problem into an argument that the entire thing is a (deliberately?) misleading ‘narrative’ created by NGOs.

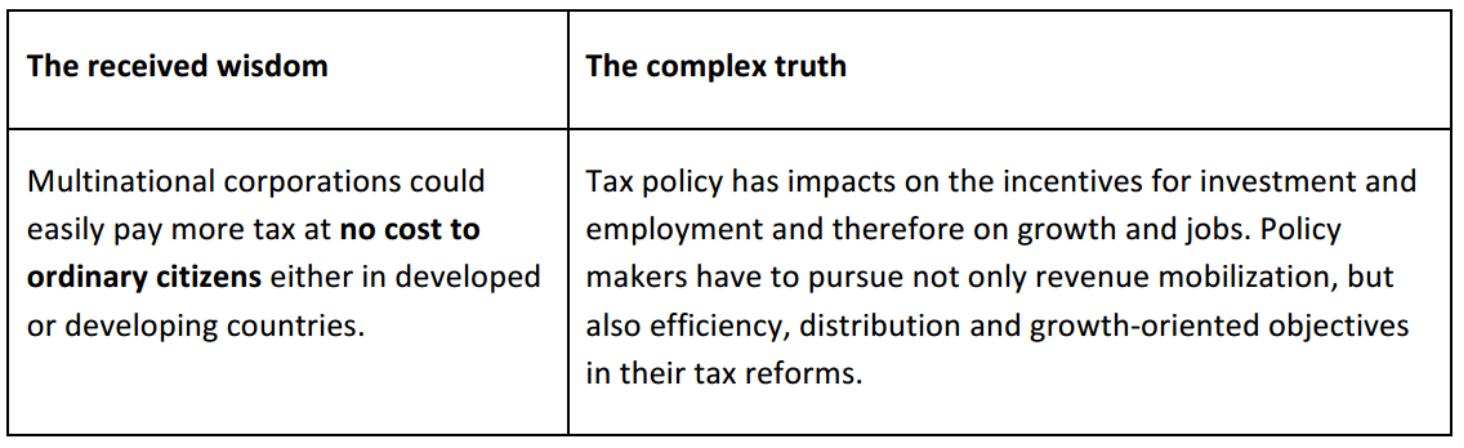

Idea 3: Money for nothing

Perhaps anticipating the reader’s scepticism by this stage, this section begins by noting: “Examples of this belief are rarely seen as direct statements” – this much is certainly true – “but often reflected in the implicit assumptions behind calculations of lost taxes…” (p.18).

The TJN quote offered as supporting evidence is intriguing:

“…tax-sensitive investment is by definition the least useful stuff: accounting nonsense and paper-shuffling that does not involve very much employment creation at all.”

Intriguing for two reasons. First, it doesn’t seem to bear directly on the ‘received wisdom’ claim. But second, because the missing start of the sentence is “But as Section 3.3 explains…” And section 3.3 includes a short literature survey with six references on the incidence and impact of corporate tax. Neither the survey nor any of the references are cited in the draft paper.

Instead, the main thrust of this brief section of the paper is to emphasise that (higher effective) corporate taxes can have negative dynamic effects. A selective survey of a few papers supporting some of these leads to the following conclusion:

“These arguments then, are not reasons to give up on taxing corporations, or necessarily to lower corporate tax rates, but underline the need for tax policy to be supported by economic analysis, rather than based on the assumption that there is ‘money for nothing’” (p.18).

If you believe in the existence of this particular ‘received wisdom’, even without any direct evidence being presented, then this is presumably a useful counter-point: we should be more careful to recognise the wider impacts of taxing corporate profits.

In any case, that’s hard to argue with – so hard, in fact, that you want to ask who would argue to the contrary? Here’s the implicit straw man that the paper has constructed:

“Tax policy should not be supported by economic analysis, but instead be based on the assumption that there is ‘money for nothing’.”

There may be a group of people who believe this (or there may not); and if there were, such a group might object to ‘the complex truth’ of policymakers actually having multiple objectives.

But if there is such a group, it presumably has little overlap with those people and NGOs like TJN that have been researching and advocating over the last fifteen years for a tax policy agenda based on economic analysis, rather than one that ignored the growing reality of abusive multinational tax practices; and for the importance of taking into account multiple objectives such as distribution.

It’s disappointing, and difficult to understand, that the paper would seek to attribute this straw man to those people and NGOs.

Summary: Straw men

It’s hard to see the contribution of this main section of the paper. The ‘complex truth’ with respect to idea 1 is a set of assertions lacking evidence, while any remaining objections to the ‘received wisdom’ are questions of scale that must be addressed by serious research. The ‘complex truth’ in relation to ideas 2 and 3 is hardly disputed, but does not contradict the main points of the ‘received wisdom’.

So the overall effect is to suggest that NGOs hold, or have promoted, extreme or unnuanced views that somehow contradict the known facts. That there is, if you like, in fact a received wisdom which the NGO narrative continually contradicts.

There are two main problems with this. First, the paper does not provide any serious evidence either for its own assertions (on which the entire argument hangs), or that any wrong views (disagreeing with an actually true ‘complex truth’) are in fact held or promoted by NGOs.

And second, even if a new draft were to do so – I’m just not sure that this is a useful way to make an argument: defining the righteous view, and implying that others disagree (or perhaps that they dishonestly pretend to).

That pot of gold

Ultimately, the CGD paper makes the argument that NGOs have exaggerated the ‘pot of gold’ that developing countries could obtain by better taxation of multinationals.

To be upfront on this, I share something of this concern. Specifically, I think the balance of attention here, compared to other aspects of tax systems, has not always been right. (At the same time, I can see good arguments for emphasising this aspect in certain policy situations.)

What do we actually know about the size of that pot though? Notwithstanding all the uncertainties discussed, and the importance of new data and continuing to improve methodologies, the best guess at the moment is probably somewhere near the latest IMF researchers’ piece: that developing country annual revenue losses might be around $200 billion, or north of 1.5% of GDP. Given average total tax revenues less than ten times that size, it’s a pretty big pot. (And all without mentioning the trend for rising shares of profits to GDP, and generally stable or falling corporate income tax revenues…)

That doesn’t mean the pot is all obtainable, or that important advances in other areas aren’t also possible, and clearly we need country-level analyses to understand the specific possibilities. But on the CGD paper’s terms, and in respect of its central claim, this is a decent pot of gold. And not one that rests on the work (or the word) of NGOs, if that’s a concern.

So if we put the mischaracterisation of the narrative, and the role of NGOs aside, the central claim of the paper just does not stand up well itself.

My final sadness about the paper is this. The last section proposes some recommendations for NGOs to improve their ways of working that are really worth discussing.

It may be difficult to move towards positive engagement based on their inclusion in a paper that makes this kind of sustained integrity attack, but I hope it may somehow prove possible to take the conversation forward in a different context.

Last thought: Does it matter?

Despite the claim to be serving the cause of better evidence and clearer debate, the draft paper muddies the waters on the potential revenue benefit from improved taxing of multinationals in developing countries – even as the evidence base has recently been further strengthened.

The timing of its being published, at the kick-off of the Financing for Development conference – the best UN opportunity in years (ever?) to lock in greater policy space for the taxing of multinationals by developing countries – is unfortunate.

The Center for Global Development is an important development think tank, and so this paper, even in draft, may well catch the attention of policymakers at Addis. And while CGD publish individual views rather than institutional ones, this may be seen as more than an individual view because it comes from a CGD process with an advisory group.

For the avoidance of doubt, I don’t think there’s any agenda at CGD – so I guess the content of this paper, its timing and any potential impact on FFD progress is just bad luck.

I very much hope that the final draft of the paper, if indeed there is one, will be quite different. A removal of the most polarising claims, where these are made on the basis of limited or no evidence, would be a good start. What would be valuable instead is a concerted examination of the data and methodologies that have been used for various aspects of revenue loss and other IFF estimates, in order to point the way forward to a strengthening evidence base over time. I hope this is a possibility; but I fear the paper may end up as a missed opportunity to contribute to an important policy research debate.

But: be not downhearted: there is substantial policy focus around the world on taxing multinationals, the research field is healthy and the agenda for new work is plentiful!

What we measure affects what we do; and if our measurements are flawed, decisions may be distorted…. [I]f metrics of performance are flawed, so too may be inferences we draw.

The UN Secretary General was told two years ago by the 2012–13 High Level Panel of Eminent Persons on the Post-2015 Development Agenda that any follow-up to the Millennium Development Goals (MDGs) had to include adata revolution.

In common with the UN global thematic consultation on inequality earlier in 2013, the High Level Panel recognised that challenging inequalities and better data collection are inextricably linked – because better data make it clear which goals are and are not being met, and because with better data we can all demand answers and action.

So the data revolution can only be about changing the balance of power. Yet much of the current discussion emphasizes purely technical reforms instead. Whilst there is nothing wrong with bringing in these new systems, such as those created by Couchbase and similar companies, it is how these technologies are used that should be considered.

I use the term ‘Uncounted‘ to describe a politically motivated failure to count that reflects power. It ignores people and groups at the bottom of distributions whose ‘uncounting’ adds another level to their marginalisation. It ignores people at the top whose uncounting hands them even greater power.

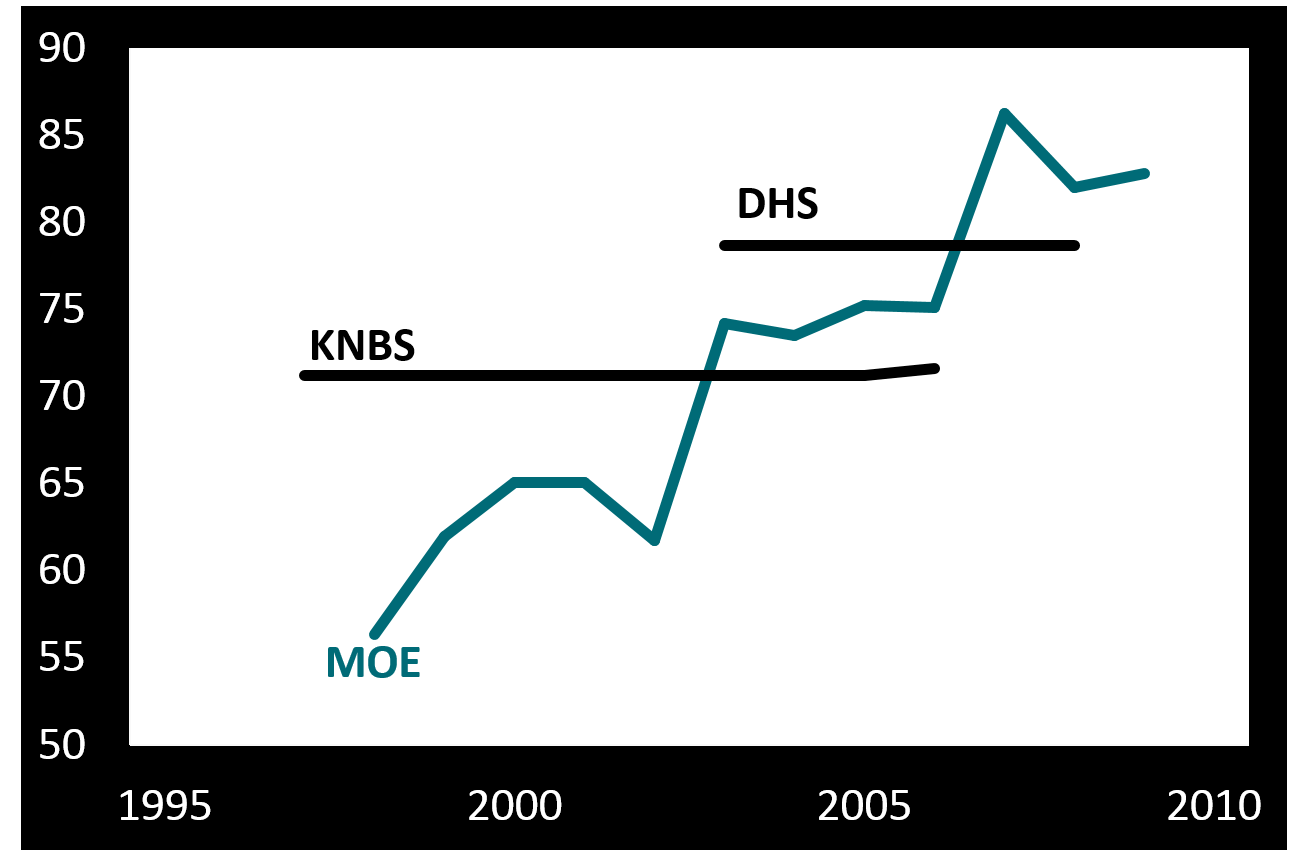

Why do we fail to count well at the bottom? This figure shows three different series for primary school enrolment in Kenya. One comes from the Kenyan National Bureau of Statistics (KNBS); one from the Demographic and Household Surveys (DHS); and one from the Ministry of Education (MOE). MOE data come directly from schools and are used as the basis for funding decisions.

Now, MOE trends tell you that progress is rapid and unsustained, while surveys look static. Which do you believe? If your children are in Kenyan state education, how well counted do you feel?

Not that survey data are perfect either. Six groups are systematically excluded from most household survey and census returns. Excluded by design are the homeless, those in institutions and nomadic populations. Ignored by undersampling are those living in fragile, disjointed households, in areas facing security risks and in informal settlements. In any research survey, there should be careful consideration of the demographic and picks for sampling. A study of various sampling methods, along with ample research into other areas of surveying, can help improve results. A large part of the populace that usually gets overlooked can then be better helped. These groups, thought to amount to around 250 million uncounted people – roughly 3.5% of today’s global population – obviously contain a disproportionate share of the world’s poorest people. They are being systematically failed even in the ‘best’ counting approaches we have.

It’s no coincidence that people in poverty are excluded. Nor is it because of technical problems that Sudan’s government in Khartoum suppresses publication of data on regional development outcomes. Or that the deaths of those living with disabilities in the UK go uncounted.

As for counting at the top, it’s equally no coincidence that high-income households are undersampled in surveys. Or that even when tax data are used to adjust the picture, major wealth – $8 trillion? $32 trillion? – remains uncounted. Or that the OECD, charged with measuring the ‘misalignment’globally between the profits of multinational companies and the actual location of their economic activity, has so far been unable to lay its hands on the necessary data.

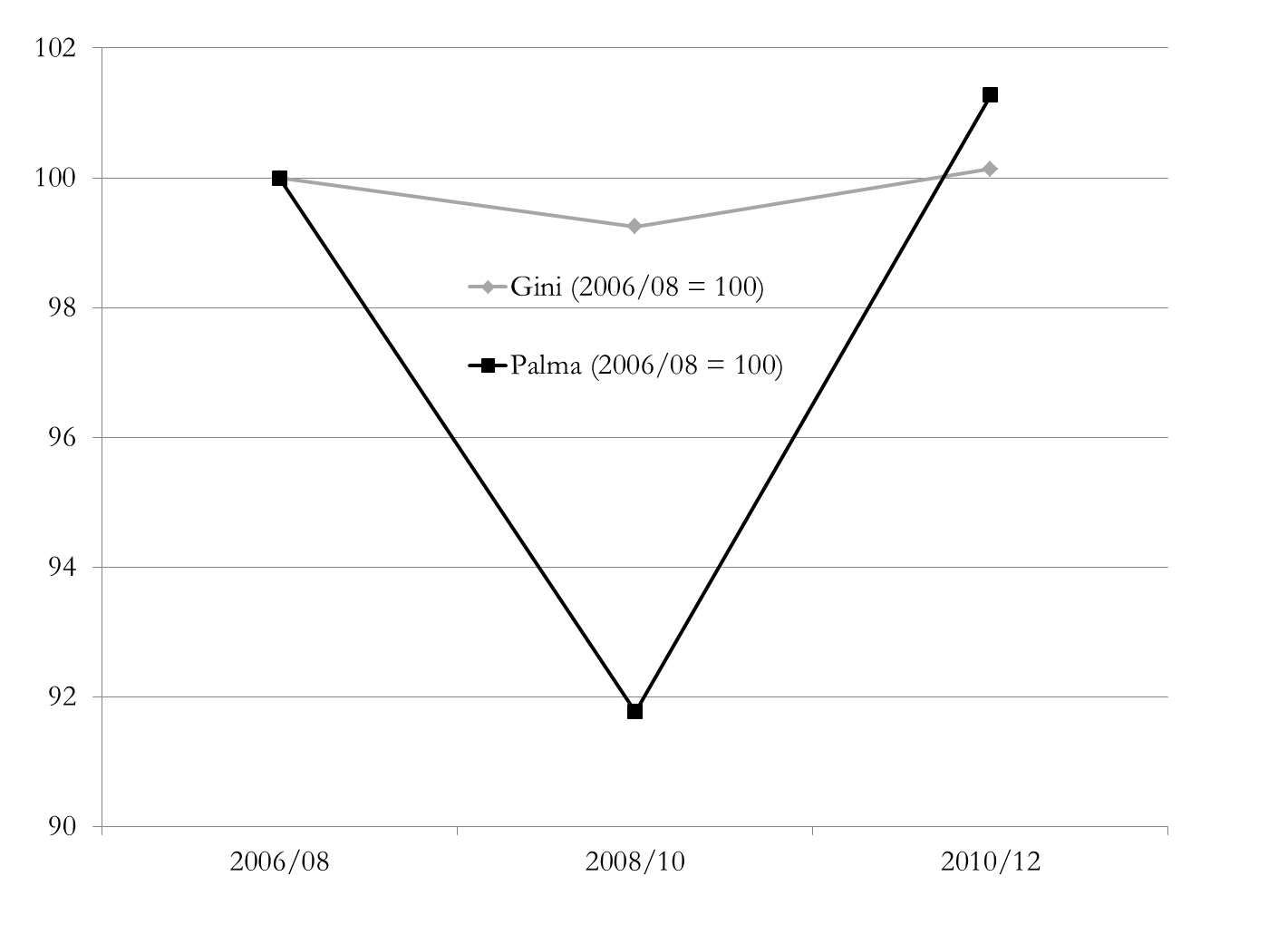

Our choice of measure is also important – and also political. Take a look at this chart which shows how two measures, the Gini coefficient and the Palma ratio, come up with radically different answers to the same question about income distribution. Has UK wealth inequality been flat across the crisis? Or did it fall sharply, then immediately rebound even more dramatically?

The Gini coefficient embodies such strong normative views (pp. 129–144) that it doesn’t capture well changes in the top 10%, or in the bottom 40% where most poverty lies. It is very encouraging (to me!) that instead the Palma ratio has featured in recent drafts of the post-2015 indicators.

The Palma – which expresses the ratio of income shares of the top 10% to the bottom 40% – also embodies a normative view, but it’s absolutely explicit about it. The chart of UK wealth distribution across the financial crisis shows why the Gini gave rise to so many congratulatory headlines about stable inequality, and why they’re wrong.

What might an actual ‘data revolution’ look like? If there’s no recognition of the political nature of the problem, then we’d be fooling ourselves to expect any great change: the same people and the same things will continue to go uncounted.

What’s noticeable in the discussion so far is that there has been a great deal more attention paid to the uncounted at the bottom than at the top. There’s been precious little mention of Piketty’s proposal for a global wealth register, for instance, or of specific measures that would eliminate anonymous company ownership, require states to exchange tax information with each other (think SwissLeaks), or multinational companies to publish country-by-country reporting (think LuxLeaks). Yet if we don’t start counting things that make elites uncomfortable, then we’re not doing it right.

Data reforms are, broadly, welcome; but a revolution remains far off. People and things go uncounted largely for political, not technical reasons.

That’s why a data revolution is so badly needed. And revolutions aren’t technical: they’re political.

February 2015. The (marginally late) Tax Justice Research Bulletin is out, the second in TJN’s monthly series dedicated to tracking the latest developments in policy-relevant research on national and international taxation.

This issue looks at new papers modelling LuxLeaks (the impact of small states competing for foreign direct investment through deliberately lax transfer pricing approaches); and on the inequality impact of the financial sector. The Spotlight looks at a range of approaches to measuring and estimating the extent of tax non-compliance – are the wealthy more likely to evade tax?

Backing track from Fela Kuti, with thanks to Joe Stead – over at TJN.

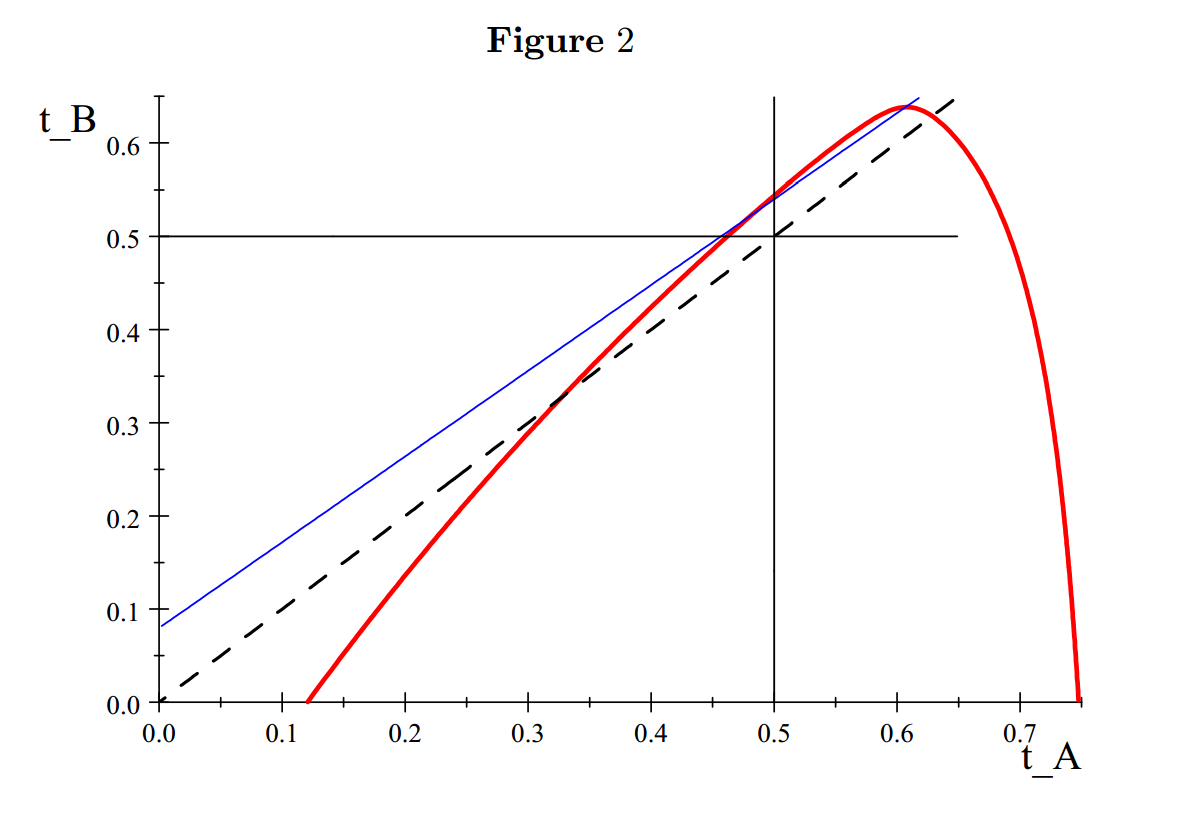

The industrial economics literature on FDI has tended to separate two elements: where multinational enterprises (MNEs) decide to locate, and where profit is subsequently declared. On the location question, the 1999 model of Haufler & Wootton has been influential. This shows that ‘competition’ between states to attract FDI, using tax breaks and subsidies, is likely to result in most or all of the benefits of the investment being captured by the MNE; but the market size advantage of a larger state ‘may even’ allow it to charge a positive tax rate and still attract the investment.

A new paper by Ma & Raimondos-Moller challenges this finding, by including the potential for profit-shifting as a factor in the location decision. Unsurprisingly, perhaps, this changes the set of possible equilibria in favour of a smaller state which is willing and able to apply transfer pricing rules more leniently – that is, to make it easier to shift in profits arising from economic activity located elsewhere.

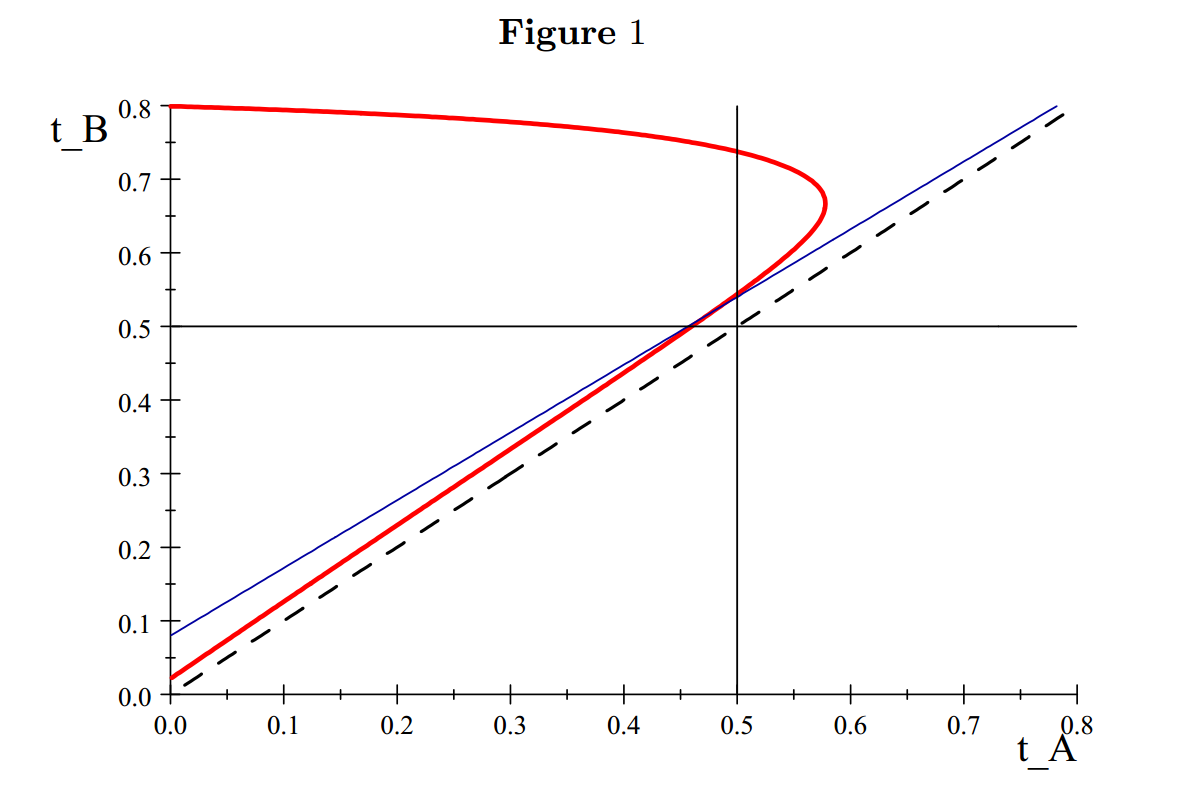

Figures 1 and 2 show the position facing the MNE, in terms of the tax rates in the small country (t_A) and in the large country (t_B). The dotted black 45° line shows where these are equal. The blue line represents the iso-profit curve in the Haufler & Wootton model. Because this is above the 45° line, the MNE is only indifferent between investing in country A or country B if the former has a lower tax rate – so the large country can have a positive tax rate and still be more attractive.

The new (red) isoprofit line in Figure 1 shows that allowing for profit-shifting reduces the large country’s advantage – the red line is closer to 45° line in the cases of interest (tax below 50%). But the striking finding is the shift of the red line in figure 2, once ‘competition’ on transfer pricing laxness is included. Now for most likely tax rates, the isoprofit line has flipped to lie below the 45° line – so that the MNE will be indifferent about location only when the large country offers a lower tax rate than the small country, because the small country’s profit-shifting advantages now outweigh the market size advantage of the large country.

Of course a model is only a model, and inevitably lacks complexity. In this case, there is obvious scope for improvement. It is assumed that the location decision is ‘real’, so that locating in the small country (say Luxembourg) will imply transport costs in order to service the large country market (say the UK); and it is also treated as an either/or decision. In practice the structure in Luxembourg is unlikely to have any contact with physical product, and the decision is likely to be both/and. (TJN’s work shows the extent of the divorce, most strongly in Luxembourg, between profits declared and real economic activity.)

Nonetheless, the paper is important. As Ma and Raimondos-Moller point out, it is the first time that profit-shifting has been incorporated in MNE location decision modelling. We can surely look forward to further developments on similar lines, including empirical testing.

Much of the #SwissLeaks data has been in the hands of tax authorities for 5 years. Many of the questions raised relate to individuals and to particular regulators and governments – but there’s also a broader question that goes to the type of solutions that will address the broader loss of trust in tax authorities’ effectiveness and independence. Clear policy changes are needed to recover trust and accountability.

If there’s a broader lesson here – and there is! – it’s that providing data privately to tax authorities is insufficient. The leaked data provided privately to (mainly European) governments in or around 2010 simply failed, in different ways, to deliver accountable and effective taxation.

Exhibit I: UK. Since receiving details of more than 1,000 cases in 2010, the UK has undertaken 1 (one) prosecution. The coalition government that came to power in 2010 also negotiated a very bad agreement with Switzerland that TJN had shown beforehand would not only protect tax evaders from transparency and prosecution but would also fail to bring in anything like the claimed sum of revenue. In addition, the government appointed as a Lord and trade minister Stephen Green, who had been the chief executive and then chairman of HSBC during the entire period.

Exhibit II: Greece. Somewhat further down the road of accountability is Greece, where the then minister of finance is now facing charges of “attempted breach of trust at the expense of the state and improperly interfering with a document”, for alleged actions relating to the loss of the list received from France, and the possible removal of relatives’ names.

Exhibit III: India. As of last month, The Indian Express reports that 15 people were facing prosecution out of more than 600 names provided by France in 2011. Today, they have published data from #SwissLeaks relating to 1195 names.

Exhibit IV: USA. Here the questions relate, once more, to what action exactly followed from the 2010 receipt of leaked data from France – and whether HSBC should have been allowed to maintain its banking licence. As The Guardian notes, no reference to the case features in the HSBC settlement of nearly $2bn relating to sanctions-busting activities.

Exhibits V and VI: Denmark and Norway. With thanks to @FairSkat and @SigridKJacobsen respectively, both of these countries with a relatively strong reputation for fair taxation did the ‘inexplicable’ and chose not to request the data from France. In the wake of the #SwissLeaks story, both now seem likely to.

Without confidence in fair and accountable taxation, governments risk the erosion not only of wider tax compliance, but of state-citizen relations and so of effective democracy (see e.g. recent behavioural and cross-country studies on the important role of tax).

That doesn’t necessarily mean that individual taxpayer data should be in the public domain. While some countries go to this length, many consider it a serious violation of privacy.

What sort of transparency is needed for accountable taxation?

How can governments (re)build trust that the rich and powerful – not to mention the criminal – will not simply go uncounted behind closed doors?

Here’s a suggestion – comments welcome:

Publish data on the aggregate bank holdings in other jurisdictions of residents, as declared by the banks and through automatic information exchange between jurisdictions (in effect, the national components of the locational banking data collected but not published by the Bank for International Settlements, which was called out by the Mbeki panel and African Union last week);

Publish data on the equivalent, as reported by taxpayers;

Publish regular updates on the status towards resolution of any discrepancy, e.g. “three cases accounting for 27% of last year’s discrepancy are now being prosecuted; investigations continue into 154 cases which account for a further 68%; while further work is underway to determine the nature of the remainder of the discrepancy (5%).” Addendum: @AislingTax points out quite rightly that I need another category here: the ‘gap’ which is not a gap, but rather relates to other features of the tax system such as non-doms in the UK.

A parallel case is that of the watering down of proposals for country-by-country reporting by multinational companies. Publication is necessary so that companies are held to account for abuses, but also so that tax authorities (and governments) are held to account for fair and effective taxation.

Private provision of this data to tax authorities may allow them to tax companies more effectively, but does nothing to demonstrate to citizens if such an opportunity is actually taken. Much of the #Luxleaks data was available to tax authorities, in theory or in practice, but only publication has led to a policy response.

As I twoth last night, the lesson of #SwissLeaks is that accountability demands public transparency.

#swissleaks lesson? Providing data privately to (OECD) tax authorities is insufficient. Greater transparency needed for accountable taxation

Aside from lurid revelations about individual companies and the big four accounting firms, the leaks of multinationals’ tax deals with Luxembourg confirm—and expose to a wider audience—the true nature of the tax ‘competition’ that prevents the emergence of effective international rules.

#Luxleaks

The International Consortium of Investigative Journalists published the second tranche of leaked files, showing tax agreements the big four accounting firms reached, on behalf of their clients, with Luxembourg. The general pattern is of establishing internal corporate finance companies in Luxembourg and using these to shift in billions of dollars of profits earned elsewhere, after obtaining confidential rulings from officials that ensure a very low effective tax rate — in many cases less than one percent.

The ICIJ’s reporting and detailed analysis of documents on individual companies from Disney to IKEA is outstanding. It clearly shows a systematic pattern of behaviour in Luxembourg, and adds to a range of other evidence suggesting the pattern is systematic across multiple jurisdictions.

Widespread tax base poaching

Several recent examples show other countries doing deals knowingly to shift in, and not (fully) tax, profits that arose elsewhere. The European Commission has initiated proceedings against Ireland for allegedly providing “State Aid” to Apple since the 1990s through unjustifiably beneficial tax treatment. This had effectively capped the level of profit Ireland would recognize as tax base, leaving untouched the vast majority of profit shifted in. Meanwhile, a more formalized version of this approach dating back 10 years, Belgium’s system of ‘excess profits rulings’, has also come under scrutiny.

In all three cases—Luxembourg, Ireland, and Belgium—the pattern is consistent. Companies, through their big four accounting firm advisers, have obtained advance agreement not to tax profits that arise, but are not taxed, elsewhere.

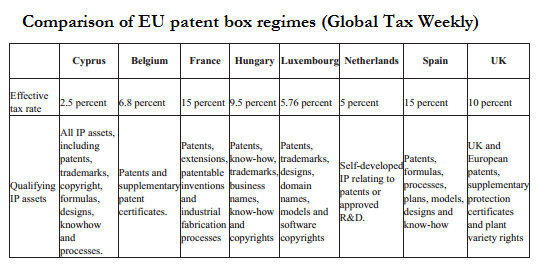

A less blatant but increasingly common instrument is the patent box, or knowledge box, which provides a very low tax rate in relation to R&D. There are already generous tax breaks for R&D in most countries. A patent box can, controversially, allow one country to capture the tax base associated with the R&D that was supported by taxpayers in another.

Such tax incentives for intellectual property exist in Belgium, Cyprus, France, Hungary, Ireland, Luxembourg, Netherlands, and Spain. In addition, the UK, which had introduced the measure from 2013, recently bowed to German pressure to phase it out (albeit not fully until 2021). The decision came after initially resisting, along with Luxembourg, Netherlands, and Spain, the suggestion that the tax break should only apply to R&D actually carried out in the country offering the patent box.

Google tax

Less than a month after its compromise over the patent box tax break, the UK government proposed a measure designed to protect its own tax base against similar poaching. The ‘diverted profits tax’ (DPT), now subject to public consultation, seeks to ensure profit arising from sales in the UK do not escape taxation by claiming to have no permanent establishment in the UK, nor through ‘certain arrangements which lack economic substance’. Perhaps unsurprisingly, given criticism of theapparent disconnect between Google’s UK profitability and tax payments, media are calling the measure the ‘Google tax’.

The expected revenue impact is small. Despite a marginally penal rate of 25 percent (compared to a standard 21 percent), the forecast is to raise around £1.3 billion over five years. The highest forecast annual take of £350 million implies a base of £1.4 billion of ‘diverted’ profits, which is equivalent to just 1.4 percent of the most recent quarterly UK corporate profits. (The basis for these estimates hasnot been published.)

The change of direction may nonetheless be important. During his announcement of the DPT, UK Chancellor George Osborne stressed “the government’s commitment to an internationally competitive tax system.” However, the DPT reflects an understanding that, too often, countries are competing not to attract real economic activity but only the taxable profit that arises from activity taking place in another jurisdiction.

The tension between playing this game, while trying to limit the counter-success of others, in large part explains the failure to develop more effective international rules – and hence the tilting of benefits towards multinationals rather than to (especially lower-income) states. Still, pressure is growing, and the eventual direction of travel will have important implications for developing countries. A companion post explores future scenarios for international tax rules, and the implications for developing countries.